Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

The Z Score Mean Reversion strategy is a statistically-grounded, counter-trend Expert Advisor (EA) for MetaTrader 5 that fades price extremes back toward a moving-average "fair value." Its primary tool is the z-score — a statistical measure of how far the current price has stretched away from its average, expressed in units of standard deviation (a gauge of how volatile recent prices have been). When price becomes statistically extreme relative to its own recent behaviour, the strategy looks to trade in the opposite direction, betting that the stretch will snap back rather than continue.

Mean reversion is the trading style at the heart of this approach. Rather than following momentum, it assumes that in range-bound conditions, prices tend to oscillate around a central mean and that unusually large deviations are more likely to correct than extend. To avoid the classic weakness of counter-trend systems — fighting a genuine trend — the strategy layers several confirmation filters on top of the raw z-score: a Relative Strength Index (RSI) exhaustion check, a "flat-regime" gate that only permits trades when the average is roughly horizontal, and a reversal-tick requirement so it never enters while price is still accelerating away.

As a learning tool, the Z Score Mean Reversion EA is well suited to traders who want to study how statistical thresholds, multi-filter confirmation, and disciplined risk exits fit together in a single system. It is a strategy analysis worth understanding for its structure and logic — not a shortcut, and not a guarantee of any particular outcome. Treat it as a framework for learning how mean-reversion logic behaves across different markets.

How It Works

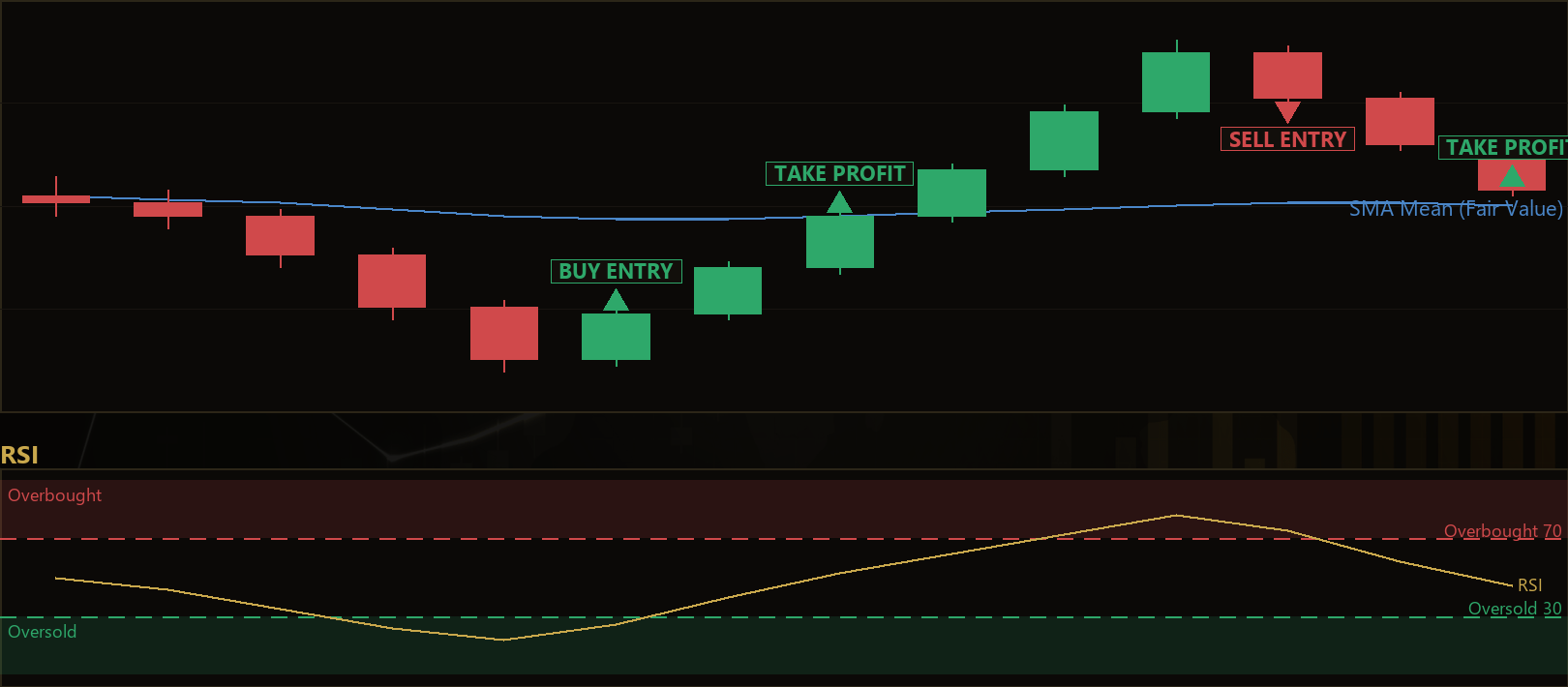

The strategy evaluates its rules once per completed bar on whatever single timeframe you attach it to. Long and short logic are fully symmetric — the short rules simply mirror the long rules. Here is how the strategy signals an entry:

- Statistical stretch (z-score): The strategy computes the mean (a Simple Moving Average) and the standard deviation of recent closes. It then measures the z-score — how many standard deviations the current close sits away from the mean. A long signal requires the z-score to fall to or below the negative threshold (price stretched well below the mean); a short signal requires it to rise to or above the positive threshold (price stretched well above the mean).

- RSI exhaustion filter: The RSI must confirm that the move is exhausted. For longs, RSI must be below the oversold level; for shorts, it must be above the overbought level (calculated as 100 minus the oversold level). This helps the strategy avoid fading a move that still has strength behind it.

- Flat-regime gate: The strategy compares the current mean to the mean from several bars ago. Only if the mean has barely moved — its change is smaller than ATR multiplied by the slope factor — does it consider the market "flat" enough to fade. This gate is designed to keep the EA standing aside during strong trends, where bands keep expanding and reversion trades tend to fail.

- Reversal tick: The most recent close must already be turning back toward the mean (a higher close for longs, a lower close for shorts). This rule is intended to avoid catching a "falling knife" on the same bar it is still dropping.

When all conditions align, the strategy signals a single position (one at a time per magic number). Exits are handled by three mechanisms:

- Stop-loss: Placed at the entry price minus (for longs) or plus (for shorts) ATR multiplied by the SL multiplier. Average True Range (ATR) measures recent volatility, so the stop adapts to how active the market currently is.

- Take-profit: Set symmetrically at ATR multiplied by the TP multiplier from entry, so the reward target scales with volatility.

- ATR break-even: Once price has moved in the trade's favour by the break-even trigger distance (in ATR units), the stop is moved to the entry price to protect against a reversal.

- Time-stop: If a trade has not resolved within the maximum number of bars, it is closed and released — a reversion that fails to occur is not left to drift indefinitely.

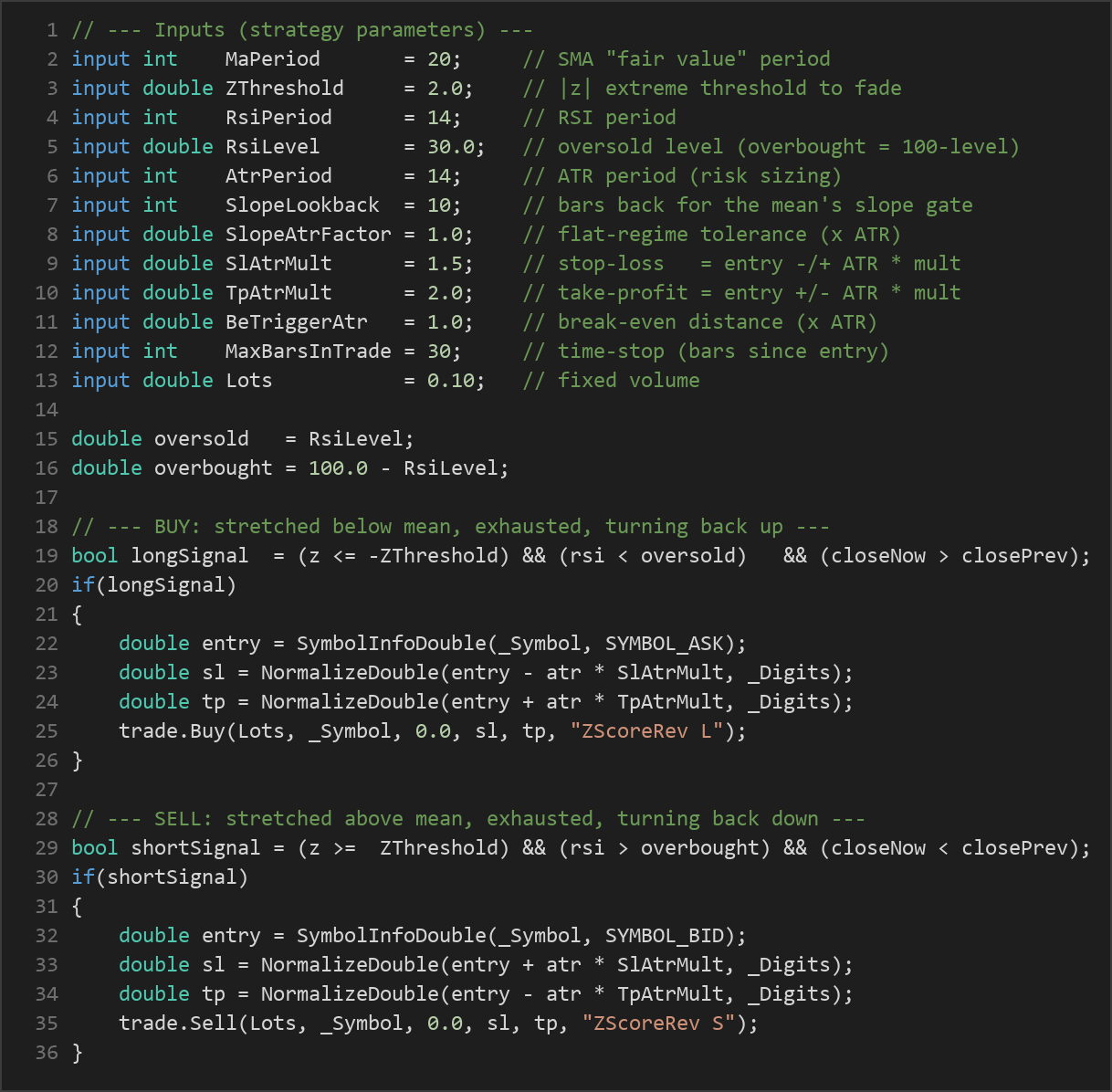

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| MaPeriod | 20 | 10 | 60 | Period of the Simple Moving Average used as the "fair value" mean and for the standard-deviation calculation. |

| ZThreshold | 2.0 | 1.0 | 3.5 | The extreme z-score (in standard deviations) that must be reached before the strategy fades the move. |

| RsiPeriod | 14 | 7 | 30 | Look-back period for the RSI exhaustion filter. |

| RsiLevel | 30.0 | 15.0 | 45.0 | Oversold level for longs; the overbought level for shorts is derived as 100 minus this value. |

| AtrPeriod | 14 | 7 | 30 | Period of the ATR used to size stops, targets, break-even, and the flat-regime gate. |

| SlopeLookback | 10 | 3 | 30 | Number of bars back used to measure the mean's slope for the flat-regime gate. |

| SlopeAtrFactor | 1.0 | 0.2 | 3.0 | Flat-regime tolerance: how much the mean may drift (in ATR units) and still count as a range. |

| SlAtrMult | 1.5 | 0.5 | 4.0 | Stop-loss distance from entry, as a multiple of ATR. |

| TpAtrMult | 2.0 | 0.5 | 5.0 | Take-profit distance from entry, as a multiple of ATR. |

| BeTriggerAtr | 1.0 | 0.3 | 3.0 | Favourable move (in ATR units) required before the stop is pulled to break-even. |

| MaxBarsInTrade | 30 | 5 | 120 | Time-stop: maximum number of bars a trade may remain open before it is released. |

| Lots | 0.10 | 0.01 | 1.0 | Fixed trade volume in lots. |

Recommended Chart Settings

The Z Score Mean Reversion EA is designed to run on a single timeframe of your choosing, applying its full rule set to whatever chart it is attached to. Mean-reversion logic tends to be studied most naturally on intraday timeframes such as M15, M30, or H1, where ranges form and resolve frequently enough to observe the strategy's behaviour. For instrument selection, range-prone markets — such as major forex pairs during quieter sessions — are a common testing ground for reversion approaches.

Because the strategy sizes its stops and targets from ATR, it adapts to each symbol's volatility automatically, but that does not make any single setting universally appropriate. Results will vary considerably across different symbols, timeframes, and market conditions. Always test a configuration on the exact chart you intend to use before drawing any conclusions.

How to Install on MetaTrader 5

- Download the .ex5 file from the link below

- Copy it to your MT5

MQL5\Expertsfolder - Restart MetaTrader 5 or refresh the Navigator panel

- Drag the EA onto a chart matching the recommended symbol and timeframe

- Configure the input parameters and enable Algo Trading

What to Consider Before Using This EA

Every strategy has trade-offs, and understanding them is part of using any EA responsibly.

Strengths of this approach. The Z Score Mean Reversion strategy is disciplined by design. Its multi-filter stack — z-score extreme, RSI exhaustion, flat-regime gate, and reversal tick — is built to reduce false signals rather than maximise the number of trades. The ATR-based stops and targets adapt to volatility, the break-even mechanism helps protect trades that move in your favour, and the time-stop prevents a stalled position from lingering indefinitely. These are sound structural features for studying how a counter-trend system manages risk.

Known limitations. Mean reversion carries an inherent weakness: when a genuine trend develops, "extreme" prices can become more extreme, and fading them repeatedly can lead to a series of losing trades. The flat-regime gate is intended to mitigate this, but no filter is perfect, and strong breakouts can still catch a reversion system offside. The strategy also trades one position at a time, so it may sit idle for long stretches waiting for all conditions to align.

Where it may underperform. Trending markets, high-impact news events, and sudden volatility spikes are the conditions where counter-trend fading historically struggles most. Because entries depend on several simultaneous conditions, the EA may generate relatively few signals, and the quality of those signals depends heavily on parameter tuning for the specific market. This is a tool for learning and analysis, not a set-and-forget solution.

Risk Management Tips

Sound risk management matters more than any single indicator setting. Consider these general principles as you study this or any strategy:

- Position sizing: Keep your trade size proportional to your account. Many educational sources suggest risking no more than 1–2% of your account balance per trade so that a losing streak does not do lasting damage.

- Understand drawdown: Every strategy experiences losing periods. Know how large a peak-to-trough decline you can tolerate emotionally and financially before you deploy any system.

- Use a demo account first: Test the EA thoroughly on a demo or backtest environment before considering any live capital. This lets you observe its behaviour across different conditions without financial exposure.

- Never over-leverage: Leverage amplifies both gains and losses. Use it conservatively and understand how margin requirements affect your account.

- Plan for the worst case: Assume trades can and will lose. A robust plan focuses on surviving bad runs, not just capturing good ones.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: ZScoreMeanReversion.ex5 (4 downloads)

- Source Code: ZScoreMeanReversion.mq5 (4 downloads)

- Documentation: ZScoreMeanReversion.pdf (3 downloads)