Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

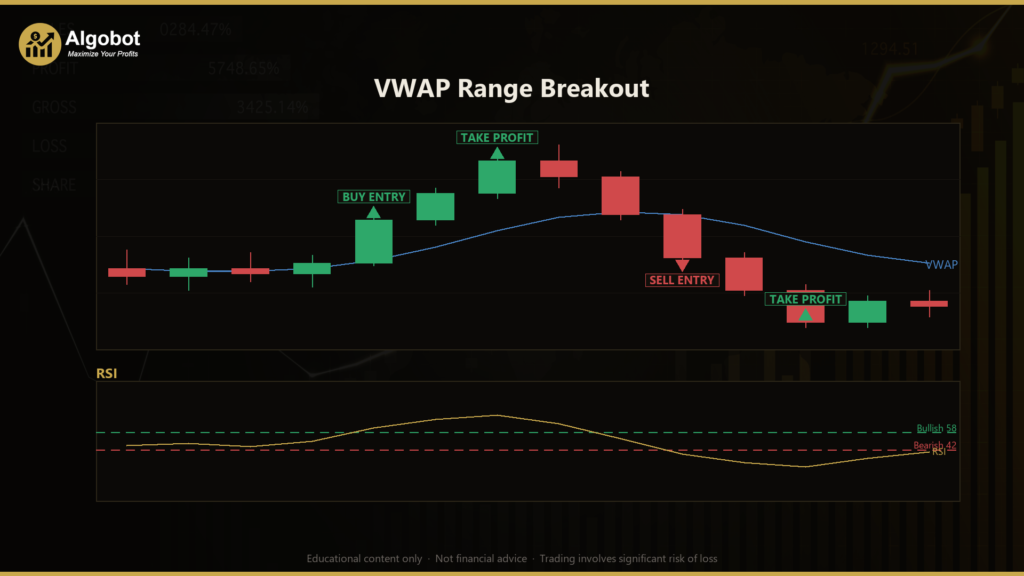

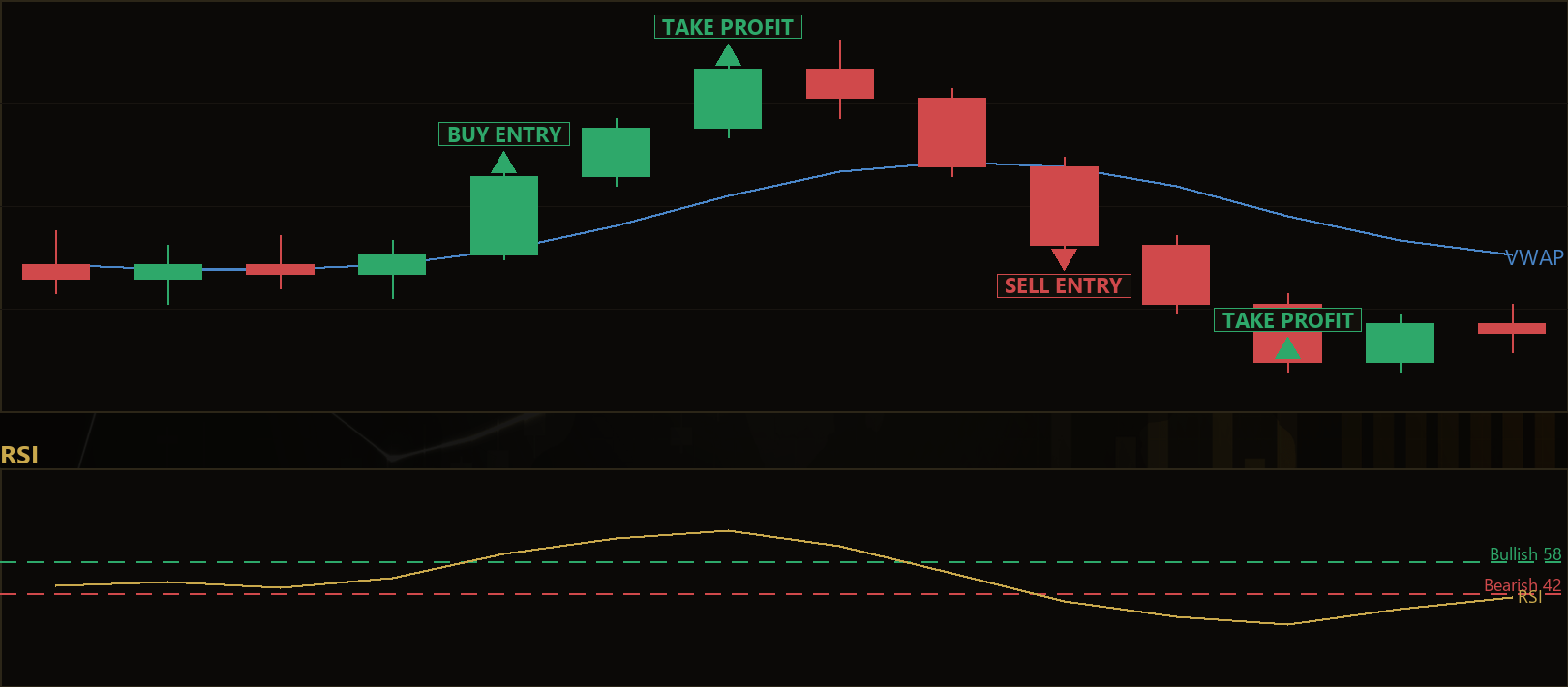

The VWAP Range Breakout strategy is a momentum-breakout system that combines a rolling VWAP (Volume-Weighted Average Price) regime filter with an N-bar price-range channel breakout and an RSI (Relative Strength Index) momentum check. VWAP is the average price of an instrument weighted by traded volume, and it is widely used by institutional desks as a "fair value" or trend anchor. The breakout pattern looks for genuine range expansion — a close beyond the recent high or low — while RSI is a 0–100 oscillator that measures the strength of recent price moves. Together these tools aim to identify the moment a market leaves a quiet range and begins to trend.

The strategy is designed for trending, momentum-driven market conditions. Breakout systems tend to struggle in flat, choppy ranges where price repeatedly pokes above a high and then falls back (a "false breakout"). To address this, the VWAP Range Breakout requires three independent confirmations to agree before it acts: price must be on the correct side of VWAP (the regime filter), price must close beyond the recent N-bar channel (the breakout), and RSI must lean in the same direction (the momentum filter). The idea is that stacking confirmations filters out many of the false signals that plague single-condition breakout systems.

As a learning tool, this strategy suits traders who want to study how multi-factor confirmation works in practice — how a trend filter, a price-action pattern, and a momentum oscillator can be combined into a single rule set. It is best treated as a framework for understanding breakout logic and trade management, not as a finished money-making product. Anyone studying it should focus on why each condition exists rather than chasing a particular outcome.

How It Works

The strategy evaluates its rules once per completed bar (candle), so it does not react to every tick. On each new bar it recalculates the rolling VWAP, RSI, and ATR, then checks the entry and exit conditions in plain sequence.

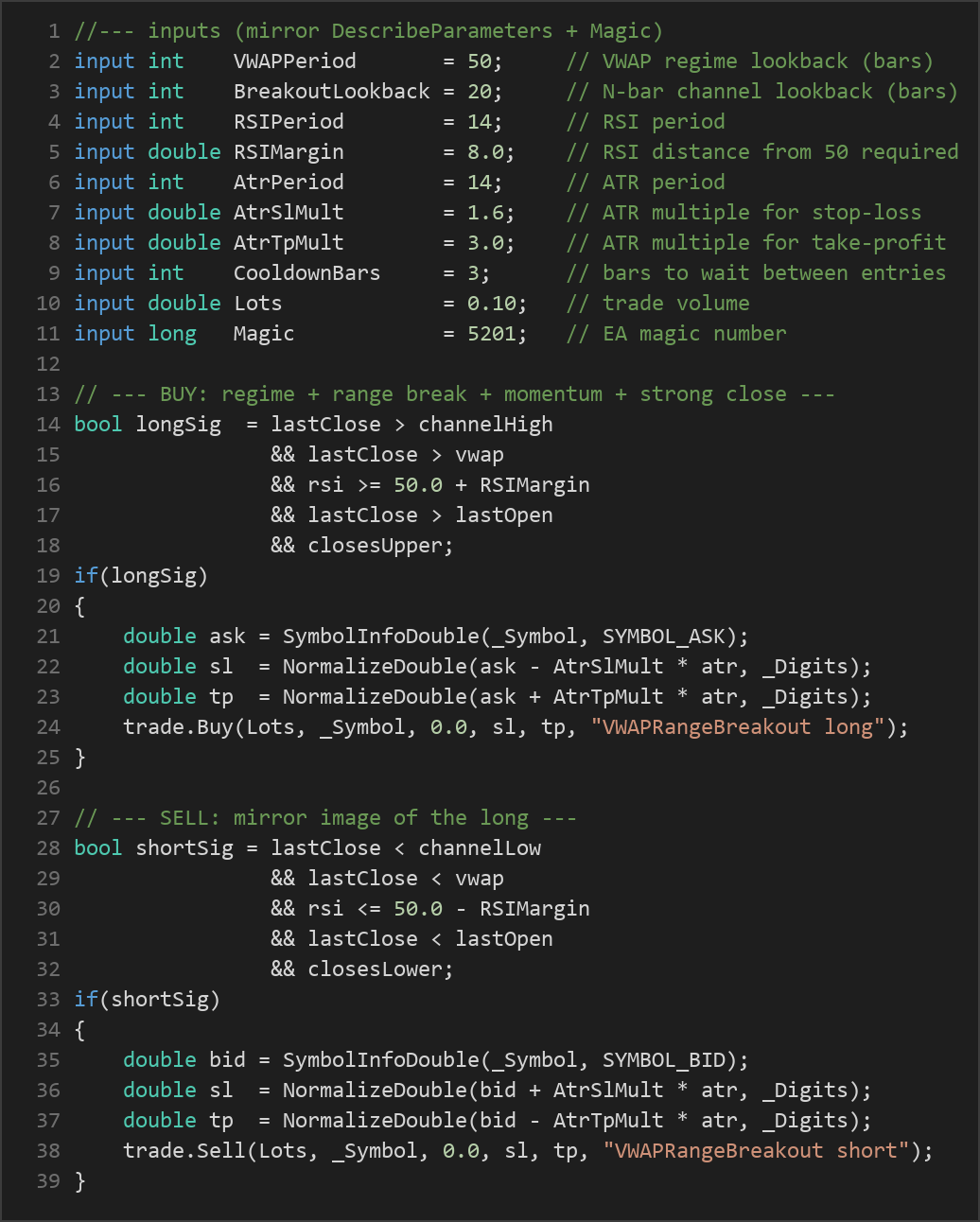

Long (buy) entry — the strategy signals a long when ALL of these are true:

- Price closes above the recent N-bar channel high, signalling genuine upside range expansion (the breakout itself).

- The closing price is above VWAP, confirming a bullish regime — price is trading above institutional fair value.

- RSI is at or above 50 + RSIMargin, indicating momentum is leaning bullish rather than neutral.

- The bar is bullish (close is higher than open).

- The bar shows a strong close near its high — the close sits in the top 40% of the bar's range, suggesting buyers stayed in control into the close.

Short (sell) entry — the strategy signals a short when ALL of these are true:

- Price closes below the recent N-bar channel low (downside range expansion).

- The closing price is below VWAP, confirming a bearish regime.

- RSI is at or below 50 − RSIMargin, indicating momentum is leaning bearish.

- The bar is bearish (close is lower than open).

- The bar shows a strong close near its low (the close sits in the bottom 40% of the bar's range).

Exit conditions:

- Stop-loss (ATR-based): When a trade opens, the stop is placed

AtrSlMult × ATRaway from entry. ATR (Average True Range) measures recent volatility, so the stop automatically widens in fast markets and tightens in quiet ones rather than using a fixed pip distance. - Take-profit (ATR-based): The target is placed

AtrTpMult × ATRaway from entry. With the default 1.6 stop and 3.0 target multiples, the structure aims for a reward-to-risk ratio of roughly 1.9 to 1. - VWAP-flip exit: If an open long closes back below VWAP — or an open short closes back above VWAP — the position is closed immediately. The reasoning is that the regime which justified the trade has disappeared, so the trade no longer has a thesis.

Trade management rules:

- One position per Magic number at a time — the strategy never stacks multiple trades on the same instrument.

- Cooldown — after a trade is opened, the strategy waits

CooldownBarscompleted bars before it is allowed to enter again, which helps avoid rapid re-entries on the same move.

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| VWAPPeriod | 50 | 20 | 200 | Number of bars used in the rolling VWAP regime filter. Larger values track a slower, longer-term fair value. |

| BreakoutLookback | 20 | 10 | 60 | Length of the N-bar channel (the recent high/low window) that price must break to trigger a signal. |

| RSIPeriod | 14 | 7 | 28 | Lookback period for the RSI momentum oscillator. |

| RSIMargin | 8.0 | 0.0 | 20.0 | How far RSI must be from the neutral 50 line before momentum is considered confirmed (e.g. 8 means ≥58 for longs, ≤42 for shorts). |

| AtrPeriod | 14 | 7 | 30 | Lookback period for the ATR volatility measure used to size stops and targets. |

| AtrSlMult | 1.6 | 0.5 | 4.0 | ATR multiple that sets the stop-loss distance from entry. |

| AtrTpMult | 3.0 | 1.0 | 8.0 | ATR multiple that sets the take-profit distance from entry. |

| CooldownBars | 3 | 0 | 20 | Number of bars to wait after a trade before another entry is permitted. |

| Lots | 0.10 | 0.01 | 1.0 | Trade volume (position size) in lots. |

Recommended Chart Settings

The VWAP Range Breakout operates on a single symbol and a single timeframe — it reads only the chart it is attached to. Because VWAP, breakout channels, and RSI all behave differently depending on the instrument's volatility and session structure, it is sensible to begin testing on a liquid major such as EUR/USD on an intraday timeframe like M15, M30, or H1, where breakout patterns and momentum tend to be cleaner. The defaults (50-bar VWAP, 20-bar channel, 14-period RSI/ATR) are general-purpose starting points rather than optimised values.

Keep in mind that results will vary considerably across different instruments, sessions, and market conditions. A setting that behaves well on one pair or timeframe may behave very differently on another, so any change should be studied on a demo account before it informs live decisions.

How to Install on MetaTrader 5

- Download the .ex5 file from the link below

- Copy it to your MT5

MQL5\Expertsfolder - Restart MetaTrader 5 or refresh the Navigator panel

- Drag the EA onto a chart matching the recommended symbol and timeframe

- Configure the input parameters and enable Algo Trading

What to Consider Before Using This EA

Strengths of this approach. The defining feature of the VWAP Range Breakout is its insistence on multiple, independent confirmations. By requiring regime (VWAP), range expansion (channel break), and momentum (RSI) to agree — plus a strong-close filter — it tends to ignore many of the half-hearted breakouts that trap single-condition systems. The ATR-based stops and targets adapt to current volatility instead of relying on fixed distances, and the VWAP-flip exit gives the strategy a logical reason to leave a trade early when its underlying thesis breaks.

Known limitations. Every filter that removes false signals also removes some genuine ones. In strongly trending markets the strict five-part entry can keep the strategy on the sidelines while price runs without it. Breakout logic is also inherently vulnerable to whipsaws in sideways, low-volatility ranges, where price may close just beyond a channel only to reverse. Because the rolling VWAP here resets to a fixed bar window rather than an exchange session, its values will differ from the traditional session-anchored VWAP that some traders expect.

Where it may underperform. Choppy, range-bound conditions and very low-liquidity periods (such as thin holiday sessions) are the most challenging environments for breakout systems. News-driven spikes can also trigger entries that reverse sharply. None of this makes the approach invalid — it simply means the strategy has conditions it is built for and conditions it is not, and understanding that difference is the point of studying it.

Risk Management Tips

Sound risk management matters far more than any single entry rule. Consider these general principles as part of your education:

- Risk a small, fixed fraction per trade. Many educational sources suggest never risking more than 1–2% of account equity on any one position, so that a string of losses cannot do disproportionate damage.

- Size positions to your stop, not the other way around. Use the ATR-based stop distance to calculate an appropriate lot size, rather than picking a lot size first.

- Test on a demo account first. Run the strategy in a risk-free simulated environment until you genuinely understand its behaviour across different market conditions.

- Understand drawdown. Every strategy experiences losing streaks. Knowing the historical depth and duration of drawdown helps you set realistic expectations and avoid abandoning a plan at the worst moment.

- Avoid over-optimisation. Tuning parameters until a backtest looks perfect often produces results that fail to repeat on new data. Favour robust, sensible settings over curve-fitted ones.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: VWAPRangeBreakout.ex5 (3 downloads)

- Source Code: VWAPRangeBreakout.mq5 (3 downloads)

- Documentation: VWAPRangeBreakout.pdf (2 downloads)