Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

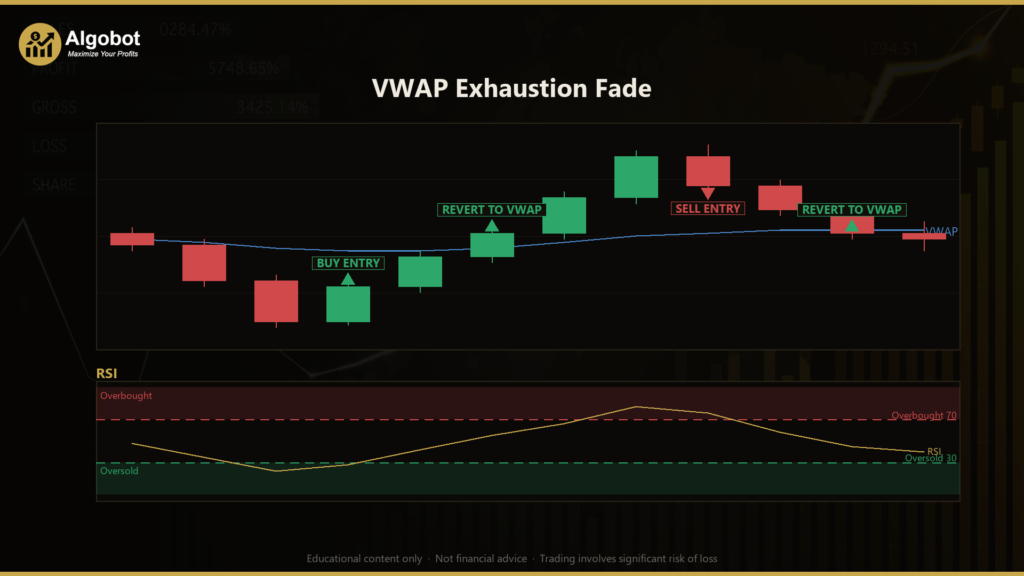

The VWAP Exhaustion Fade is an intraday mean-reversion strategy built around the Volume-Weighted Average Price (VWAP) and the Relative Strength Index (RSI). VWAP is the average price of an instrument across the trading session, weighted by traded volume — institutions treat it as a benchmark of "fair value" for the day. RSI is a momentum oscillator that measures whether price has moved too far, too fast in one direction. By combining the two, this strategy looks for moments when price has stretched an unusually large distance away from its session VWAP at the same time that momentum has reached an exhaustion extreme.

The core idea is reversion. Within a single session, price tends to be pulled back toward VWAP repeatedly, because that level represents where the bulk of volume has actually changed hands. When a move pushes price far above or below VWAP and RSI simultaneously signals that the move is overstretched, the strategy treats that combination as a sign the move may be running out of fuel. It then "fades" the move — taking a position in the opposite direction — once a confirming reversal candle prints. The exit target is the return to VWAP itself.

This is best understood as a learning tool for studying mean-reversion and confluence-based filtering, not a money-making system. It suits traders who want to see how a volatility-adaptive deviation trigger (measured in ATR, the Average True Range, rather than a fixed pip count) can be combined with a momentum filter and a candle confirmation to reduce false signals. If you are studying how institutional fair-value concepts and oscillators interact, this strategy offers a clean, readable example.

How It Works

The strategy only evaluates conditions when a bar has fully closed, so signals do not flicker on every tick. On each newly closed bar it updates a session-anchored VWAP (which resets at the start of each UTC calendar day), recalculates ATR and RSI, and then checks for either an entry or an exit.

Entry conditions — the strategy signals a long (buy) fade when all of these align:

- Price has stretched below VWAP by more than the deviation band, where the band is

DeviationAtrMult × ATR. This means the stretch is measured relative to current volatility, not a fixed distance. - RSI is at or below the oversold threshold, suggesting downside momentum may be exhausted.

- The just-closed candle is bullish (close above open), acting as a reversal confirmation.

The strategy signals a short (sell) fade when the mirror image is true:

- Price has stretched above VWAP by more than the

DeviationAtrMult × ATRband. - RSI is at or above the overbought threshold.

- The just-closed candle is bearish (close below open).

Exit conditions:

- The primary exit is the reversion to VWAP. A long position is closed once the bid reaches or exceeds VWAP; a short position is closed once the ask falls to or below VWAP. This is the mean-reversion target the strategy is designed to capture.

- A take-profit is also placed at

TpAtrMult × ATRaway from entry, and a stop-loss atStopAtrMult × ATRbeyond the extreme. These protective orders bound the trade if price never reverts to VWAP or runs further against the position.

Additional logic worth noting:

- A warm-up guard ensures enough closed bars exist before RSI and ATR are trusted.

- The

MinSessionBarssetting forces the strategy to wait a configurable number of bars into the session before VWAP is considered stable enough to fade against. - Only one position per magic number is held at a time, so the strategy will not stack multiple trades on the same signal.

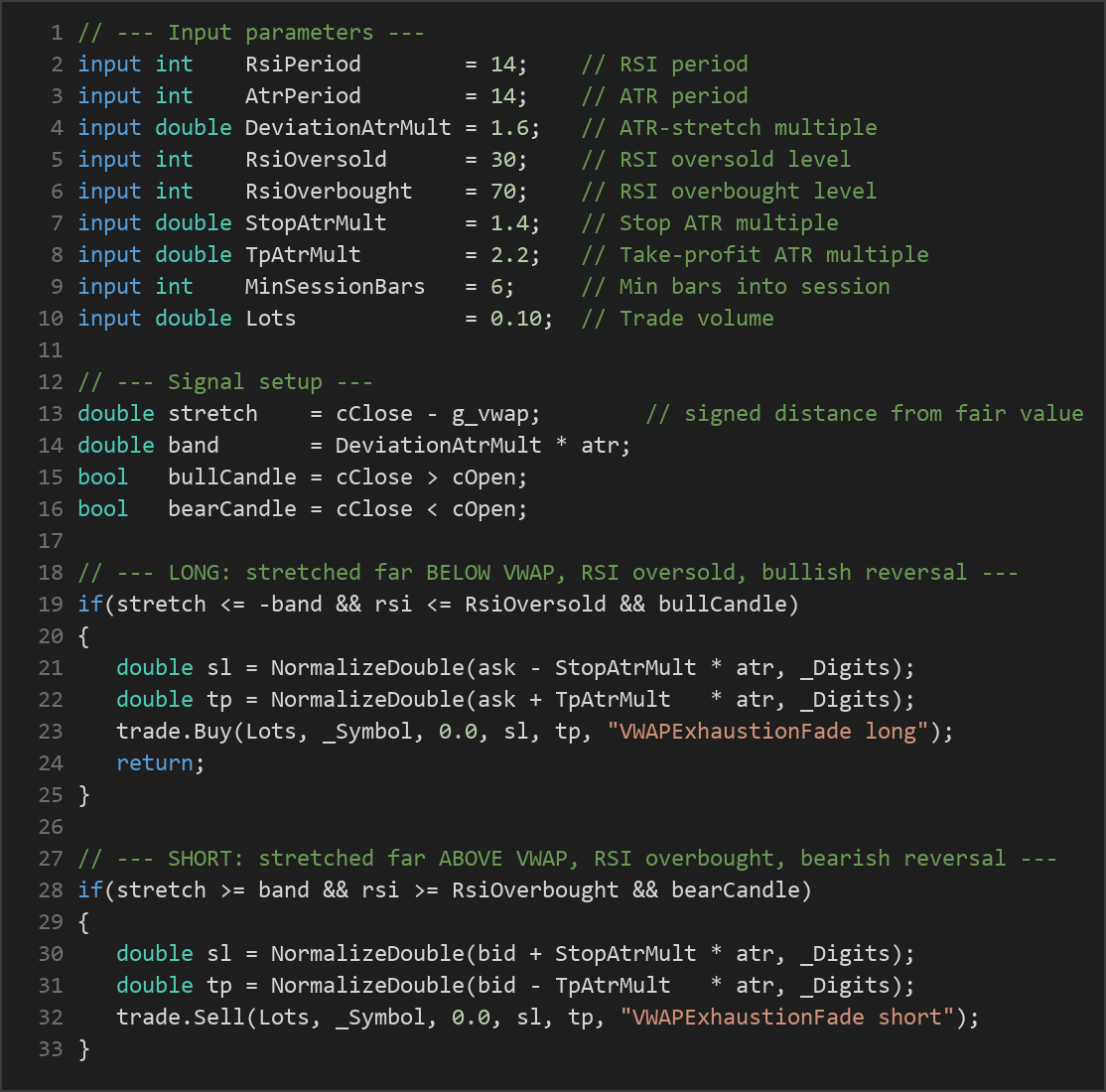

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| RsiPeriod | 14 | 5 | 30 | Lookback length for the RSI momentum oscillator. |

| AtrPeriod | 14 | 5 | 30 | Lookback length for ATR, used to size the deviation band, stop, and target. |

| DeviationAtrMult | 1.6 | 0.5 | 4.0 | How many ATRs price must stretch from VWAP before a fade is considered. Higher = stricter. |

| RsiOversold | 30 | 15 | 40 | RSI level at or below which downside momentum is treated as exhausted (long trigger). |

| RsiOverbought | 70 | 60 | 85 | RSI level at or above which upside momentum is treated as exhausted (short trigger). |

| StopAtrMult | 1.4 | 0.5 | 4.0 | Stop-loss distance from entry, expressed in ATR multiples. |

| TpAtrMult | 2.2 | 0.5 | 5.0 | Take-profit distance from entry, expressed in ATR multiples. |

| MinSessionBars | 6 | 1 | 40 | Minimum bars into the session before signals are allowed (lets VWAP stabilize). |

| Lots | 0.10 | 0.01 | 1.0 | Fixed trade volume in lots. |

Recommended Chart Settings

Because VWAP is a session-anchored, intraday concept that resets each calendar day, this strategy is designed for intraday timeframes — typically the M5, M15, or M30 charts. Lower timeframes give the session enough bars for VWAP and the MinSessionBars filter to be meaningful, while still producing several setups per session.

It is most naturally applied to liquid instruments with consistent intraday volume, such as major forex pairs (for example EUR/USD) or major indices. The tick-volume weighting used for VWAP behaves best on actively traded symbols. As always, results will vary across different symbols, brokers, and market conditions — a setup that behaves well in a ranging session may behave very differently during a strong trend or a news-driven move. Test on the specific symbol and timeframe you intend to study before drawing any conclusions.

How to Install on MetaTrader 5

- Download the

VWAPExhaustionFade.ex5file from the link below. - Copy it to your MT5

MQL5\Expertsfolder. - Restart MetaTrader 5 or refresh the Navigator panel.

- Drag the EA onto a chart matching the recommended symbol and timeframe.

- Configure the input parameters and enable Algo Trading.

What to Consider Before Using This EA

The strength of this approach is its discipline. Rather than fading every wiggle away from VWAP, it requires three conditions to align — an ATR-scaled stretch, an RSI exhaustion reading, and a confirming reversal candle. Measuring the stretch in ATR units means the trigger automatically adapts to volatile and quiet sessions instead of relying on a fixed pip count. The VWAP exit gives the strategy a logical, structure-based target rather than an arbitrary one.

The limitations are equally important to understand. Mean-reversion strategies are inherently vulnerable to strong, sustained trends: when price stretches far from VWAP and simply keeps going, an over-extension fade can be repeatedly stopped out. RSI can remain oversold or overbought far longer than expected during a powerful move, so an "exhaustion" reading is never a guarantee of reversal. The VWAP reset at the UTC day boundary may not align perfectly with your broker's session, which can affect where fair value sits early in the day. And because the strategy uses tick volume (not true exchange volume) for weighting, the VWAP is an approximation rather than an exact institutional figure.

This EA may underperform in trending markets, during major news releases, and in thin, illiquid conditions where the deviation band becomes erratic. Treat it as a framework for studying confluence and mean-reversion behavior, and observe how it responds across many sessions before forming any view.

Risk Management Tips

Sound risk management matters far more than any single set of parameters. Consider these general principles as you study this strategy:

- Position sizing: Keep trade size small relative to your account. A common educational guideline is to risk no more than 1–2% of account equity on any single trade. The fixed

Lotssetting does not scale to your balance, so adjust it deliberately. - Use a demo account first. Run the EA on a demo or backtest environment until you fully understand how and when it enters and exits. Never deploy a strategy live before you have seen it behave across varied conditions.

- Understand drawdown. Even a well-designed mean-reversion approach can string together losing trades during trending periods. Know the maximum loss you are prepared to tolerate before you begin.

- Respect the stops. The ATR-based stop-loss exists to bound risk when price fails to revert. Disabling or widening stops removes the protection the design depends on.

- One strategy is not a portfolio. Diversifying study across approaches and conditions gives a more honest picture than judging a single EA on a single symbol.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: VWAPExhaustionFade.ex5 (1 downloads)

- Source Code: VWAPExhaustionFade.mq5 (2 downloads)

- Documentation: VWAPExhaustionFade.pdf (3 downloads)