Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

The Session Vwap Rejection Reversal is a mean-reversion trading strategy built around a single reference line: the session-anchored VWAP (Volume Weighted Average Price). VWAP is the average price of an instrument over the trading session, weighted by traded volume — it represents the "fair value" that large institutions benchmark their fills against. This strategy is deliberately minimalist. It uses no RSI, no moving averages, and no ATR. The only inputs are the VWAP line, its volume-weighted deviation bands, and a price-action rejection candle at those bands.

The strategy is designed for liquid intraday markets that have a clear daily session, such as an FX major (for example EURUSD) or a stock index CFD (for example US500), typically on the M5 to M15 timeframes. The core idea is that when price stretches a long way from VWAP and then snaps back, institutional order flow is often stepping in at the extreme to defend fair value. The strategy attempts to read that snap-back footprint and trade the move back toward the mean.

As a learning tool, this approach is well suited to traders who want to understand how VWAP behaves through a session, how volume-weighted standard deviation bands are constructed, and how a clean candlestick rejection can define both a stop and a target. It is a focused case study in mean reversion rather than a trend-following or breakout system. This article is a strategy analysis — it explains the mechanics so you can study how the logic is assembled, not a promise of any particular outcome.

How It Works

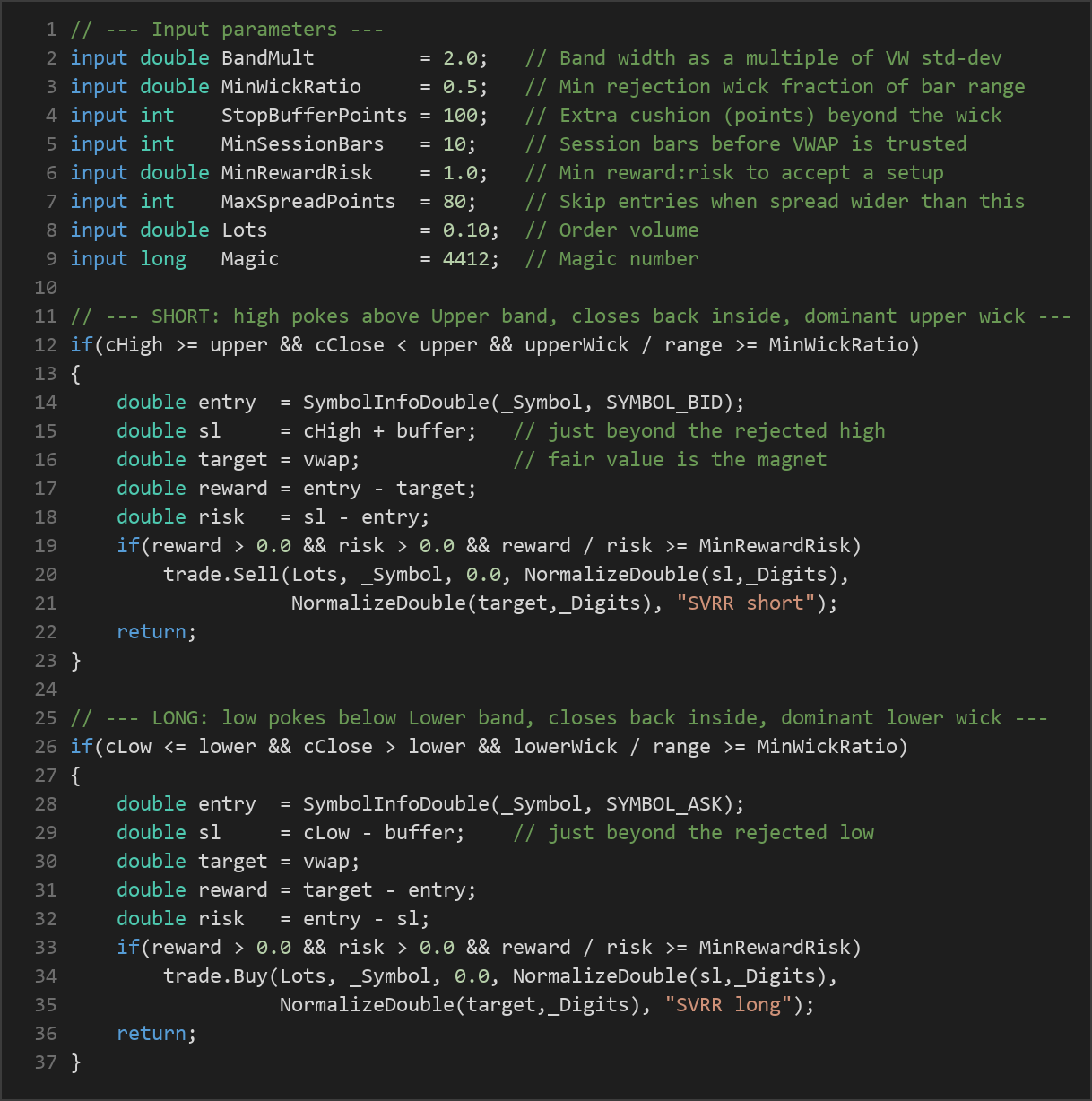

The strategy rebuilds VWAP from scratch at the start of every session (it resets its accumulators on each new calendar-day boundary) and updates it bar-by-bar as the session unfolds. On each newly closed bar it performs the following steps:

- Roll VWAP forward. Using the just-closed bar, it adds the typical price (the average of high, low, and close) multiplied by tick volume to a running total, building the cumulative VWAP and a volume-weighted standard deviation around it.

- Build the deviation bands. The upper band sits at VWAP plus

BandMultstandard deviations; the lower band sits at VWAP minusBandMultstandard deviations. These bands define how far is "too far" from fair value. - Wait for enough data. VWAP is not trusted until at least

MinSessionBarsbars have accumulated in the current session, avoiding noisy early-session readings. - Check the gatekeepers. It holds only one position per magic number at a time, and it skips new entries when the current spread is wider than

MaxSpreadPoints.

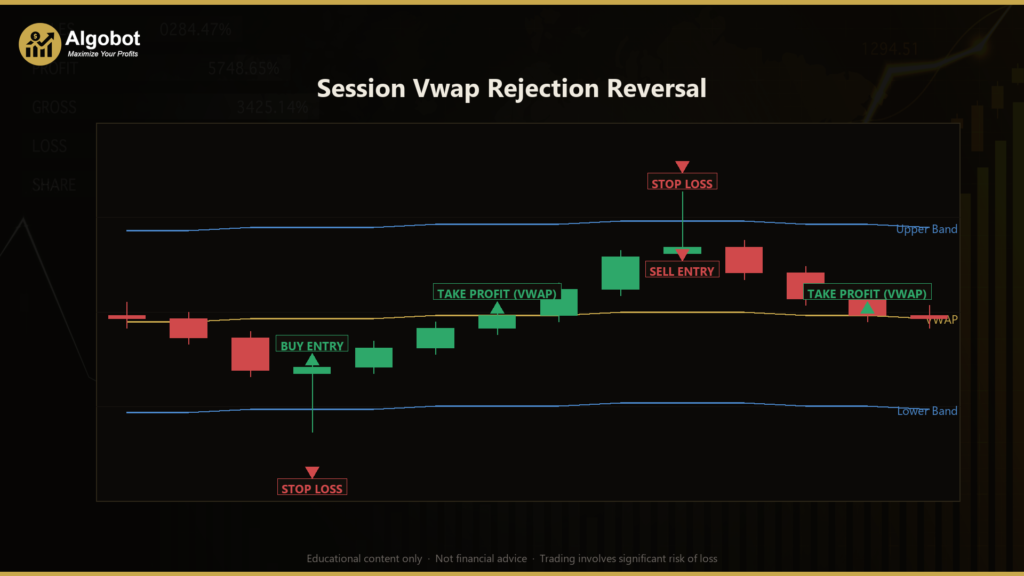

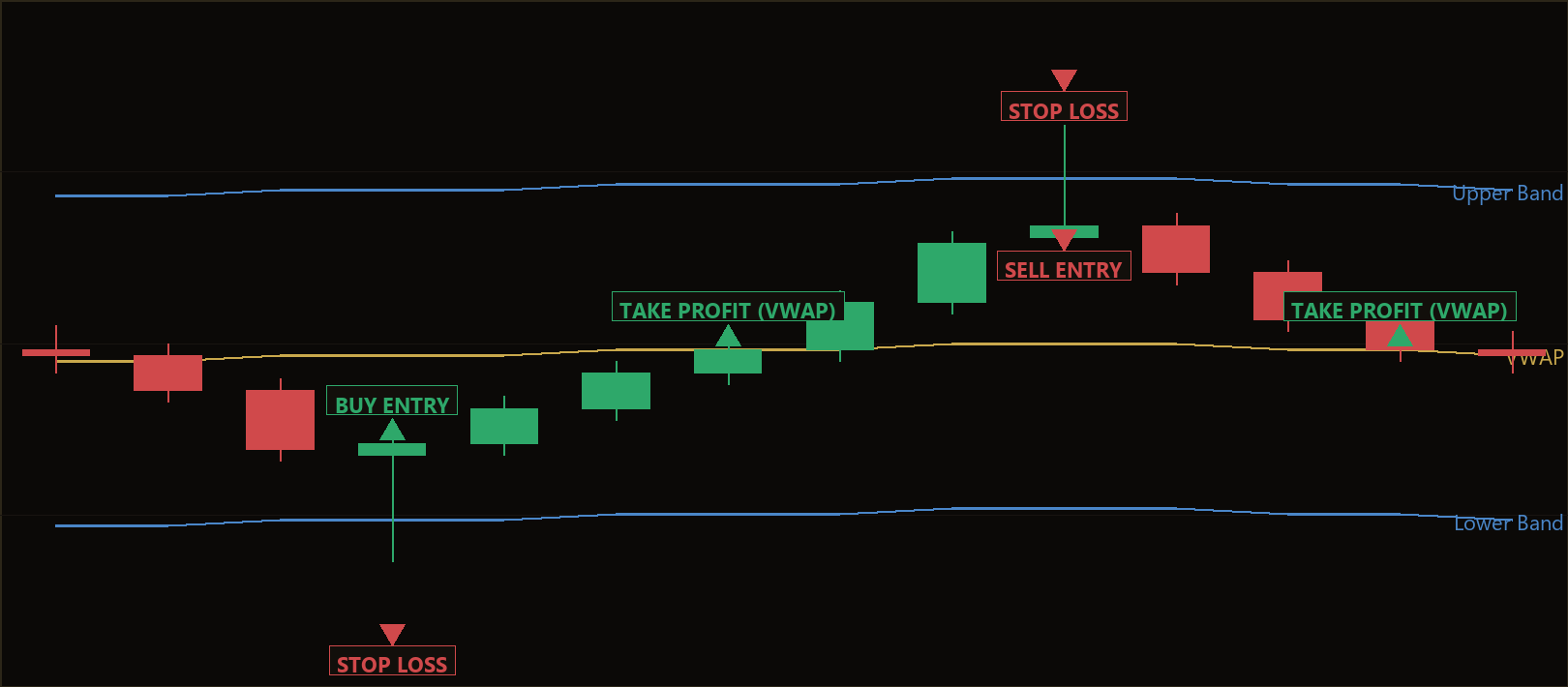

Once those conditions are met, the strategy looks for a rejection candle — a band touch alone is never traded, because over-stretched price can keep running. A rejection requires price to poke through a band with a wick and then close back inside it, with that wick dominating the bar.

- Short signal: The bar's high pierces the upper band, the bar closes back below the upper band, and the upper wick is at least

MinWickRatioof the bar's total range. The strategy signals a sell, expecting price to fall back toward VWAP. - Long signal: The bar's low pierces the lower band, the bar closes back above the lower band, and the lower wick is at least

MinWickRatioof the bar's total range. The strategy signals a buy, expecting price to rise back toward VWAP.

Stop-loss logic is structural and self-defining. For a short, the stop is placed just above the rejected high (the wick extreme that proved the band held), plus a small buffer of StopBufferPoints. For a long, the stop sits just below the rejected low, minus the same buffer. The wick that rejected the band becomes the natural invalidation level.

Take-profit logic is equally simple: the target is always VWAP itself — the "magnet" that fair value represents. Before any trade is placed, the strategy measures the potential reward (distance from entry to VWAP) against the risk (distance from entry to the wick stop). If the reward-to-risk ratio is below MinRewardRisk, the setup is rejected because price has already drifted too close to VWAP to justify the stop distance. Because only one position is held at a time, the wick stop and the VWAP target manage every exit.

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| BandMult | 2.0 | 1.0 | 4.0 | Band width as a multiple of the volume-weighted standard deviation around VWAP. Larger values demand a bigger stretch before a setup qualifies. |

| MinWickRatio | 0.5 | 0.2 | 0.8 | The rejection wick must be at least this fraction of the signal bar's total range to count as a genuine reversal. |

| StopBufferPoints | 100 | 10 | 600 | Extra cushion, in points, placed beyond the rejection wick when setting the stop-loss. |

| MinSessionBars | 10 | 3 | 60 | Number of bars that must accumulate in the current session before VWAP is trusted for signals. |

| MinRewardRisk | 1.0 | 0.3 | 4.0 | Minimum reward-to-risk ratio required to accept a setup; rejects trades where VWAP is too close. |

| MaxSpreadPoints | 80 | 5 | 400 | Skip new entries when the current spread, in points, is wider than this value. |

| Lots | 0.10 | 0.01 | 1.0 | Order volume (position size) in lots. |

| Magic | 4412 | 0 | 9,999,999 | Magic number used to identify and manage this strategy's positions. |

Recommended Chart Settings

The Session Vwap Rejection Reversal was designed with a liquid intraday market in mind — one that has a genuine daily session so that the VWAP reset is meaningful. Natural candidates are an FX major such as EURUSD or an index CFD such as US500, on the M5 to M15 timeframes. These conditions tend to provide both the volume data VWAP relies on and the intraday mean-reversion behavior the strategy is built to read.

That said, the code itself reads only the primary symbol and timeframe selected at backtest or run time, so it will operate on whatever chart you attach it to. Results will vary considerably across different symbols, timeframes, and market conditions. Always test a configuration on the specific instrument and timeframe you intend to study before drawing any conclusions.

How to Install on MetaTrader 5

- Download the .ex5 file from the link below

- Copy it to your MT5

MQL5\Expertsfolder - Restart MetaTrader 5 or refresh the Navigator panel

- Drag the EA onto a chart matching the recommended symbol and timeframe

- Configure the input parameters and enable Algo Trading

What to Consider Before Using This EA

Strengths of the approach. The strategy is transparent and easy to reason about. Because it uses a single, well-understood reference line, every decision can be traced: the band defines the stretch, the rejection wick defines the entry and the stop, and VWAP defines the target. The risk on each trade is structurally bounded by the wick extreme rather than an arbitrary fixed distance, and the minimum reward-to-risk filter screens out setups with unfavorable geometry. The spread filter and the minimum-session-bars rule add further discipline.

Known limitations. Mean-reversion systems share a characteristic weakness: they assume price will return to fair value, which is true on many days but emphatically not on strong trending or news-driven days. On a trending session, price can ride along a band and a rejection signal can be repeatedly stopped out as the move extends. The VWAP reset is tied to a calendar-day boundary, so instruments whose real trading session does not align cleanly with the UTC day may produce a VWAP that drifts before enough bars accumulate. The strategy also relies on tick volume as a proxy for true volume, which is broker-dependent in FX. Finally, holding only one position per magic means the strategy can sit idle through many setups while a single trade resolves.

Where it may underperform. Expect weaker behavior during sustained trends, around high-impact economic releases, in thin or illiquid hours when spreads widen past the filter, and on instruments without a meaningful session structure. As with any rules-based system, it is a tool for studying market behavior, not a substitute for judgment.

Risk Management Tips

Sound risk management matters more than any single signal. As an educational framework, consider these general principles:

- Position sizing: Size each position relative to your account, not to a fixed lot habit. Many educators suggest risking no more than 1–2% of account equity on any single trade.

- Use a demo account first: Study the strategy on a demo account until you understand how it behaves across trending and ranging sessions before considering any live capital.

- Understand drawdown: Every strategy experiences losing streaks. Review the maximum historical drawdown of any configuration so you know what a normal rough patch looks like, and decide in advance how much you are willing to endure.

- Respect the spread and session filters: They exist to avoid poor-quality conditions; loosening them too far can expose you to costs and noise.

- Never risk money you cannot afford to lose, and treat backtests as historical analysis rather than a forecast.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: SessionVwapRejectionReversal.ex5 (6 downloads)

- Source Code: SessionVwapRejectionReversal.mq5 (1 downloads)

- Documentation: SessionVwapRejectionReversal.pdf (4 downloads)