Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

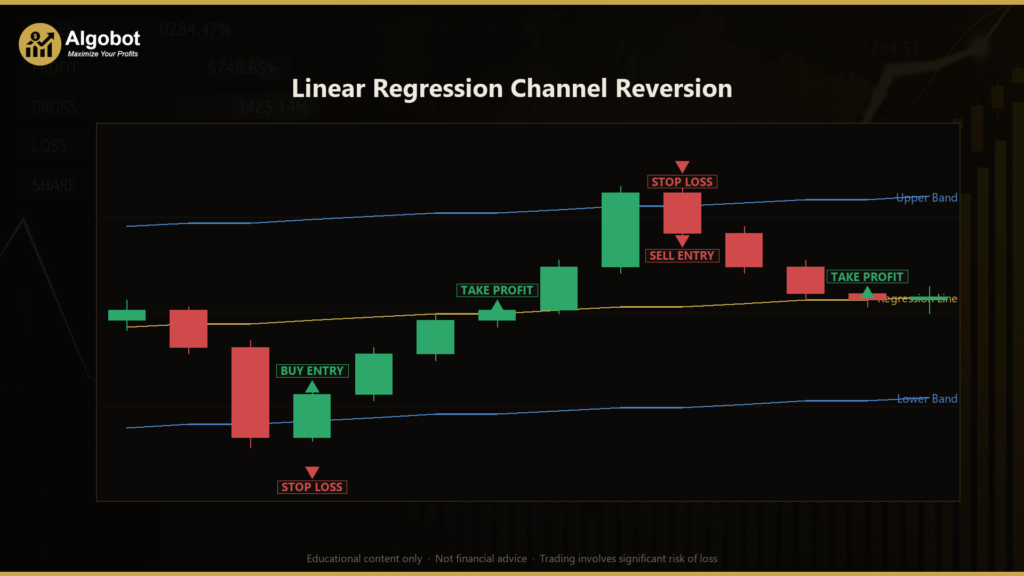

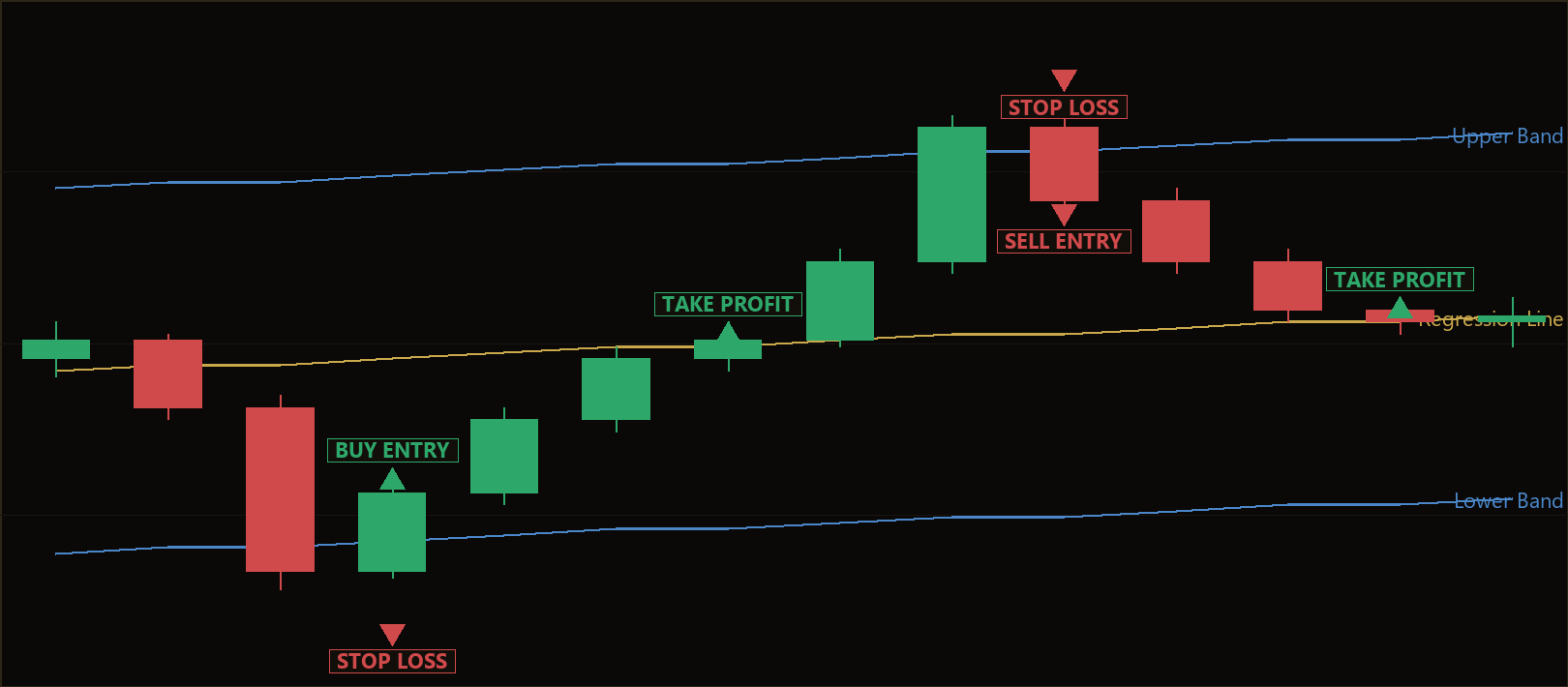

The Linear Regression Channel Reversion strategy is a mean-reversion trading system built around a least-squares linear regression channel — a statistical tool that fits the single best-fit straight line through a recent stretch of price and then measures how far price typically wanders from that line. In plain terms, the strategy treats the regression line as the market's short-term "fair value" and looks to trade price back toward it after an unusually large deviation. Mean reversion is a trading style based on the observation that price, having stretched away from an average, often gets pulled back toward it.

Rather than fitting a subjective trendline by eye, the strategy computes the regression mathematically over a fixed number of recent bars. It then builds a channel around that line using the standard deviation of price about the fit (a measure of how tightly price hugs the line). The result is an adaptive channel whose width automatically expands in volatile conditions and contracts in quiet ones. This is designed for range-bound or gently-drifting markets where price oscillates around a central value, and it is deliberately built to avoid strong, one-directional trends.

As a learning tool, this strategy is well suited to traders who want to understand how statistical concepts — regression, standard deviation, and reward-to-risk filtering — translate into concrete, rule-based entries and exits. It is best approached as a study of how a disciplined mean-reversion system is structured, not as a shortcut to returns. Every element is objective and reproducible, which makes it an excellent case study in systematic strategy design.

How It Works

The strategy acts only once per newly-closed bar and holds at most one position at a time. Here is how it forms its decisions in plain English:

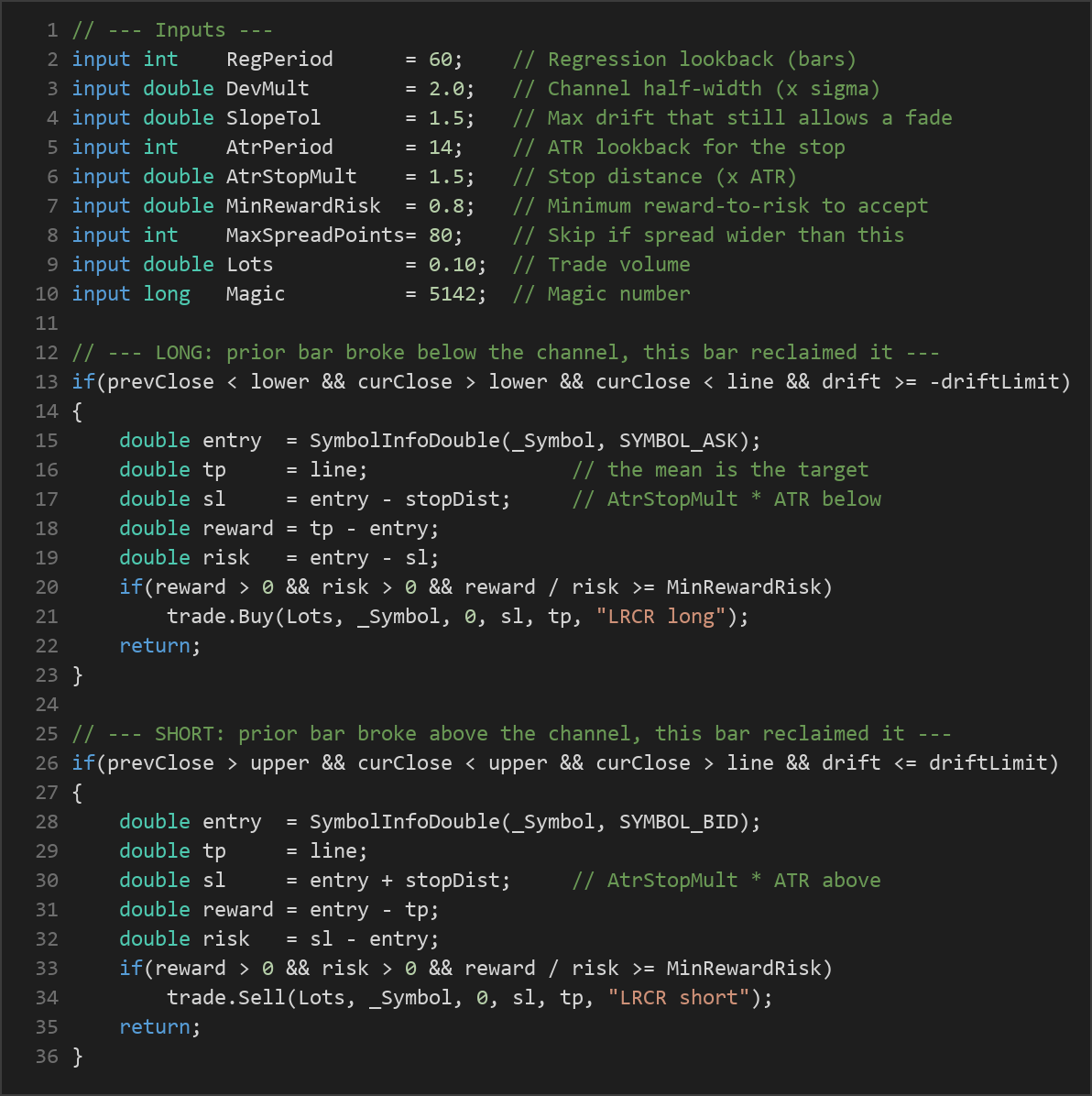

- Fitting the channel: Over the last

RegPeriodclosed bars, the strategy fits a least-squares regression line to closing prices. This line represents the estimated "mean" trajectory of price. It then calculates the residual standard deviation (sigma) — the average distance of price from that line — and places an upper and lower band atDevMult× sigma above and below the line. - Waiting for a reclaim, not a touch: A naked band touch can simply keep going, so the strategy does not fade the raw extreme. Instead it waits for a reclaim: the previous bar must have closed outside a band, and the just-closed bar must have stepped back inside it. This one-bar confirmation is the first objective sign that the deviation is being rejected.

- Long entry signal: The strategy signals a long when the prior bar closed below the lower band, the just-closed bar closed back above the lower band (but still below the regression line, leaving room to revert upward), and the channel is not steeply falling. It buys at the ask price.

- Short entry signal: The strategy signals a short when the prior bar closed above the upper band, the just-closed bar closed back below the upper band (but still above the line), and the channel is not steeply rising. It sells at the bid price.

- The slope filter: To stay out of runaway trends, the strategy measures the total drift of the channel across the window (

slope × (N-1)) in units of sigma. Longs are blocked when the channel is falling faster thanSlopeTol× sigma, and shorts are blocked when it is rising faster. This keeps trades confined to reasonably balanced, gently-sloped channels. - Take-profit logic: The target is the regression line itself — the mean. This is a genuine structural magnet rather than an arbitrary fixed distance, because mean reversion is precisely the tendency of price to return to that line.

- Stop-loss logic: The protective stop is placed

AtrStopMult× ATR beyond the entry. ATR (Average True Range) is a volatility measure, so the stop distance self-scales with current market conditions — wider when the market is choppy, tighter when it is calm. - Reward-to-risk filter: Before committing, the strategy checks that the distance to the line target is at least

MinRewardRisktimes the ATR stop distance. Setups already too close to the line are rejected as not worth the risk. - Spread filter: New entries are skipped when the current spread (in points) exceeds

MaxSpreadPoints, avoiding costly fills during illiquid or news-driven conditions.

Because the take-profit is the mean and the stop is ATR-based, the structural target and volatility stop manage every exit automatically once a position is open.

Strategy Parameters

| Parameter | Default | Min | Max | Description | ||

|---|---|---|---|---|---|---|

| RegPeriod | 60 | 20 | 200 | Lookback in bars for the least-squares regression fit and its sigma channel. | ||

| DevMult | 2.0 | 1.0 | 4.0 | Channel half-width as a multiple of the residual standard deviation. | ||

| SlopeTol | 1.5 | 0.0 | 5.0 | Maximum channel drift (\ | slope × (N-1)\ | , in sigma units) that still allows a fade. |

| AtrPeriod | 14 | 5 | 30 | ATR lookback used to size the protective stop. | ||

| AtrStopMult | 1.5 | 0.5 | 4.0 | Protective stop distance (× ATR) placed beyond the entry. | ||

| MinRewardRisk | 0.8 | 0.3 | 3.0 | Rejects setups whose line target is closer than this × the ATR stop. | ||

| MaxSpreadPoints | 80 | 5 | 300 | Skips new entries when the current spread (points) is wider than this. | ||

| Lots | 0.10 | 0.01 | 1.0 | Trade volume in lots. | ||

| Magic | 5142 | 0 | 9,999,999 | Unique identifier so the EA manages only its own positions. |

Recommended Chart Settings

This strategy was designed with liquid instruments in mind: a major FX pair such as EURUSD or GBPUSD, or a metal such as XAUUSD (gold). The intended timeframes are M15 to H1, where regression-channel reversion tends to be better behaved and intraday noise is less dominant. The EA runs on whatever timeframe is selected at backtest or attach time, so the chart period you choose directly determines the length of the regression window in real time.

Keep in mind that results will vary considerably across different symbols, timeframes, and market regimes. A channel that reverts cleanly in one period may drift persistently in another, which is exactly why the slope filter exists — and why forward-testing on your own broker's data matters.

How to Install on MetaTrader 5

- Download the .ex5 file from the link below.

- Copy it to your MT5

MQL5\Expertsfolder. - Restart MetaTrader 5 or refresh the Navigator panel.

- Drag the EA onto a chart matching the recommended symbol and timeframe.

- Configure the input parameters and enable Algo Trading.

What to Consider Before Using This EA

Every trading approach has strengths and limitations, and an honest assessment helps you learn more from studying it.

Strengths of this approach. The strategy is fully objective — there is no discretionary interpretation of trendlines. The reclaim requirement filters out many naked-touch false signals, and the slope filter helps the system sidestep the classic mean-reversion trap of fading a market that is actually trending. Because the channel width, the stop, and the target all self-scale with volatility, the logic adapts to changing conditions without manual retuning. The reward-to-risk gate enforces a minimum trade quality before any order is sent.

Known limitations. Mean-reversion systems are fundamentally vulnerable to strong, sustained trends. When a market breaks out and keeps running, price can close outside a band, briefly reclaim it, and then continue against the trade — the slope filter reduces but cannot eliminate this. The line target is not guaranteed to be reached; price may reverse before touching the mean. Fixed-lot sizing does not adjust position size to account balance, and a fixed regression window may fit poorly when the underlying volatility regime shifts abruptly. During major news events, spreads can widen beyond the filter's assumptions between bars.

Where it may underperform. Expect weaker behavior in trending or breakout conditions, during low-liquidity sessions, and around scheduled high-impact news. The strategy is designed for balanced, oscillating markets, and it will historically struggle when that assumption breaks down.

Risk Management Tips

Sound risk management is what separates studying a strategy from gambling with it. Consider these general principles:

- Risk a small, fixed fraction per trade. A common educational guideline is to risk no more than 1–2% of account equity on any single position. Because this EA uses a fixed lot size, you may need to adjust

Lotsso that the ATR-based stop corresponds to a sensible fraction of your account. - Understand drawdown. Even a well-designed mean-reversion system will experience losing streaks. Know the maximum peak-to-trough decline you are prepared to tolerate before you begin.

- Always start on a demo account. Forward-test on a demo or a very small live account across varied market conditions before considering any meaningful capital.

- Account for costs. Spread, slippage, and swap can materially affect a short-target strategy like this one. The spread filter helps, but real fills differ from ideal ones.

- Avoid over-optimization. Tuning parameters until a backtest looks perfect (curve-fitting) tends to produce results that do not hold up going forward. Prefer robust settings that work across a range of values.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: LinearRegressionChannelReversion.ex5 (4 downloads)

- Source Code: LinearRegressionChannelReversion.mq5 (3 downloads)

- Documentation: LinearRegressionChannelReversion.pdf (3 downloads)