Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

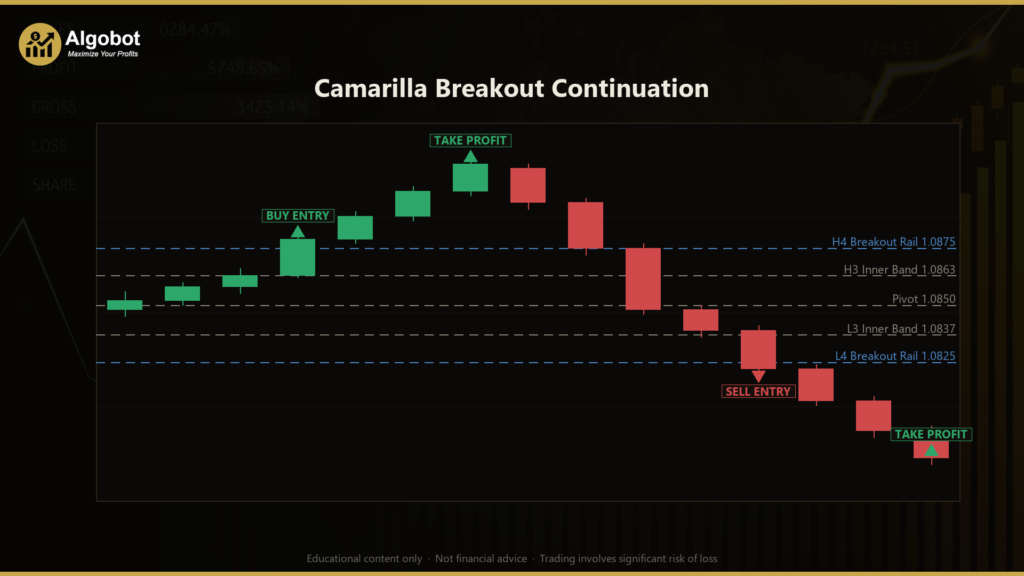

The Camarilla Breakout Continuation strategy is an intraday Camarilla pivot breakout system for MetaTrader 5 that trades in the direction of a developing "trend day." Camarilla pivots are a ladder of support and resistance levels calculated once per day from the previous day's high, low, and close. Instead of fading (trading against) the edges of the day's range like many pivot systems, this strategy waits for price to force its way through the outer rail and then joins the move, using an Average True Range (ATR) filter to screen out noise. ATR is a common volatility gauge that measures the average size of recent price bars.

The strategy is built for directional, one-sided sessions — the kind of day where price opens, pushes decisively past the day's expected range, and keeps going rather than rotating back and forth. In classic Camarilla theory, while price stays inside the inner H3–L3 band the market is considered "rotational" and traders fade the extremes. When a bar closes beyond the wider H4 (upper) or L4 (lower) rail, that rotation is judged to have failed, and order flow is treated as one-directional. This system takes the continuation side of that break.

As a learning tool, the Camarilla Breakout Continuation is well suited to traders who want to study how pivot-based levels, breakout confirmation, and volatility-adaptive risk fit together in a single rules-based framework. Because its stops and targets are defined in ATR multiples rather than fixed points, the same logic can be examined across different symbols and volatility regimes. This article is a strategy analysis — a walkthrough of the mechanics — not a profit opportunity.

How It Works

The strategy processes one action per newly closed bar on the primary timeframe. Each day it rebuilds its Camarilla levels from the prior day's data, then watches for a fresh close beyond the outer rail.

Building the daily levels:

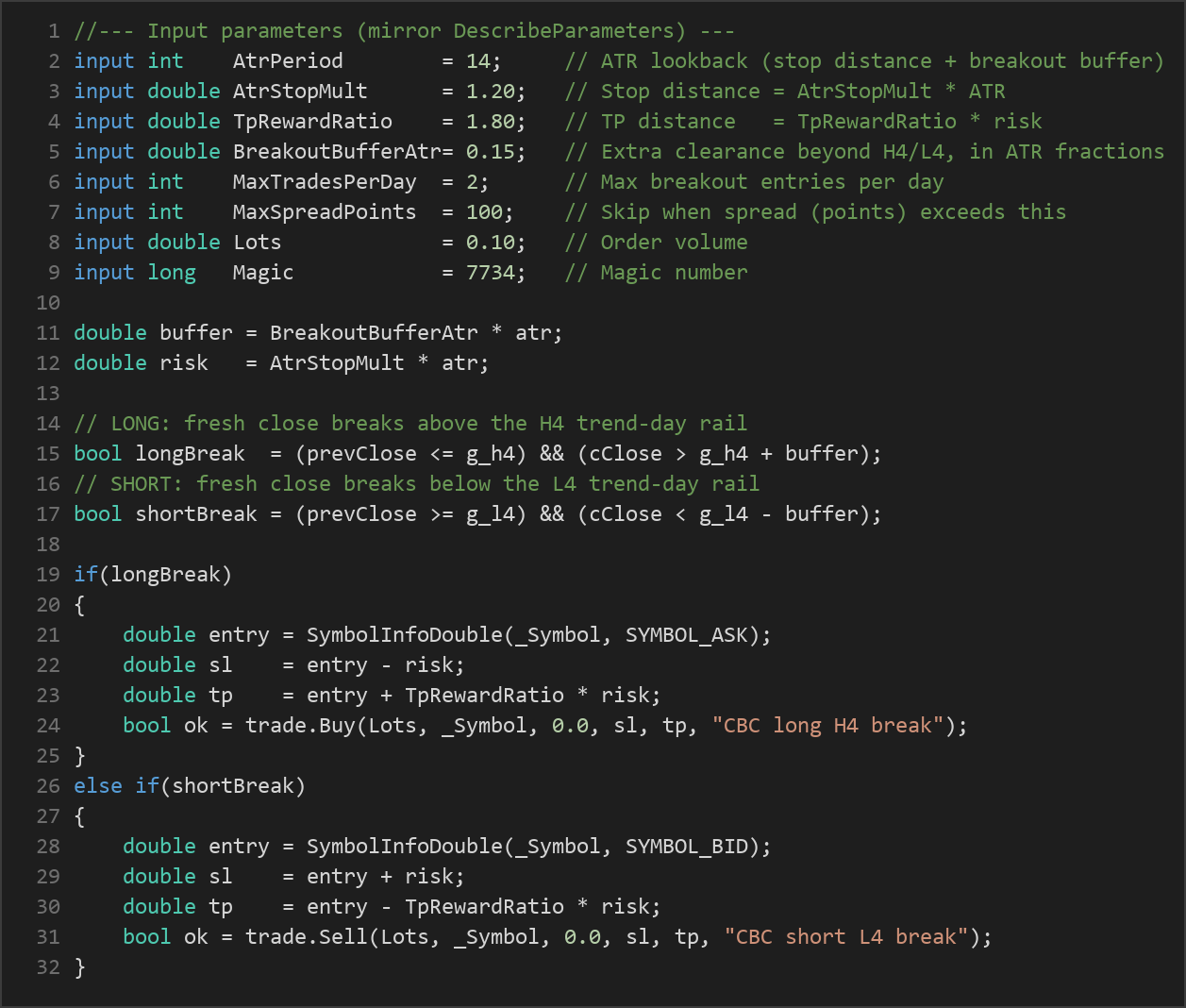

- At each new UTC calendar-day boundary, the strategy finalizes the previous day's High (H), Low (L), and Close (C), accumulated bar-by-bar from the primary timeframe itself.

- It calculates the prior day's range as

R = H − L. - The reversal/fade band:

H3 = C + R × 1.1/4andL3 = C − R × 1.1/4. - The breakout/trend-day rail:

H4 = C + R × 1.1/2andL4 = C − R × 1.1/2. - The central pivot

P = (H + L + C) / 3is calculated for context only.

Entry conditions (the strategy signals a trade when):

- Long: the previously closed bar sat at or below the upper H4 rail, and the newest closed bar closes above H4 by more than a buffer (

BreakoutBufferAtr × ATR). This "fresh cross" plus buffer is read as a genuine upside trend-day break, and the strategy buys the continuation. - Short: the mirror image — the previous close was at or above the lower L4 rail, and the newest close breaks below L4 by more than the buffer. The strategy sells the continuation.

Filters that must pass before any entry:

- The Camarilla levels for the day must already be built.

- Enough closed bars must exist to compute the ATR.

- The daily trade budget (

MaxTradesPerDay) must not be exhausted — this stops the strategy from re-firing on the same exhausted break. - No existing position may be open for the strategy's magic number (one position at a time).

- The current spread must not exceed

MaxSpreadPoints, which blocks costly fills during thin or volatile conditions.

Stop-loss logic:

- Risk is defined as

AtrStopMult × ATR. For a long, the stop is placed that distance below the entry price; for a short, that distance above it. - Because the stop is measured in ATR, it automatically widens in volatile conditions and tightens in quiet ones, without needing manual point-size tuning per symbol.

Take-profit logic:

- The target is a fixed multiple of the risk:

TpRewardRatio × risk. With the default 1.80 reward ratio, the target sits 1.8 times as far from entry as the stop, defining the reward-to-risk shape of each trade before it is placed.

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| AtrPeriod | 14 | 5 | 50 | Lookback length for the ATR used in both the stop distance and the breakout buffer. |

| AtrStopMult | 1.20 | 0.30 | 4.00 | Stop-loss distance as a multiple of ATR from the fill price. Higher values give the trade more room. |

| TpRewardRatio | 1.80 | 0.50 | 5.00 | Take-profit distance expressed as a multiple of the ATR-based risk (the reward-to-risk ratio). |

| BreakoutBufferAtr | 0.15 | 0.00 | 1.50 | Extra clearance beyond H4/L4 a close must exceed, as a fraction of ATR, to count as a genuine breakout (noise filter). |

| MaxTradesPerDay | 2 | 1 | 10 | Maximum number of breakout entries allowed within a single day. |

| MaxSpreadPoints | 100 | 5 | 400 | Entries are skipped when the current spread (in points) exceeds this value. |

| Lots | 0.10 | 0.01 | 1.00 | Fixed order volume in lots for each trade. |

| Magic | 7734 | 0 | 9,999,999 | Unique identifier so the EA manages only its own positions. |

Recommended Chart Settings

The Camarilla Breakout Continuation is a day-trading system, and Camarilla pivots are traditionally used on intraday charts. The M15, M30, and H1 timeframes are the natural homes for this approach — they are frequent enough to catch a break early yet slow enough to filter out much of the tick-by-tick noise. Because day boundaries are detected from the primary timeframe itself, the strategy runs correctly on whatever intraday timeframe you select.

The ATR-based risk model means the logic is not tied to any single instrument, so it can be studied on major forex pairs, indices, or other liquid symbols. That said, results will vary considerably across different markets and market conditions. A symbol that trends cleanly during your session may behave very differently from one that chops sideways, so treat any setting as a starting point for your own testing rather than a fixed recommendation.

How to Install on MetaTrader 5

- Download the

.ex5file from the link below - Copy it to your MT5

MQL5\Expertsfolder - Restart MetaTrader 5 or refresh the Navigator panel

- Drag the EA onto a chart matching the recommended symbol and timeframe

- Configure the input parameters and enable Algo Trading

What to Consider Before Using This EA

Strengths of this approach. The strategy is built on a well-documented, transparent concept — Camarilla pivots are a decades-old framework, and the rules here are fully mechanical, which makes them easy to study and backtest. The ATR-based stop and target adapt to volatility automatically, so the same logic behaves sensibly whether a symbol is quiet or active. The fresh-cross requirement plus the ATR buffer are deliberate attempts to avoid entering on every minor poke through a level, and the per-day trade cap and spread filter add discipline that many manual traders struggle to maintain.

Known limitations. Breakout systems are, by design, prone to false breakouts: price can close beyond H4 or L4, trigger an entry, then reverse straight back into the range. This is the classic failure mode for any level-break strategy, and it tends to cluster on quiet, rotational days — exactly the conditions Camarilla theory says favor fading rather than following. The buffer reduces but cannot eliminate these whipsaws. The strategy also assumes the previous day's range is a meaningful guide to today's behavior; after news events, gaps, or holidays, that assumption can break down.

Where it may underperform. Range-bound, low-volatility sessions may indicate an environment where continuation breaks repeatedly fail. Very wide spreads, illiquid symbols, or erratic overnight sessions can also degrade fills. Historically, trend-following breakout methods experience long stretches of small losing trades punctuated by occasional larger winners, so the distribution of outcomes can feel uneven even when the underlying logic is sound. Understanding that shape is part of using this kind of system responsibly.

Risk Management Tips

Sound risk management matters far more than any single entry rule. Consider the following general principles as you study this strategy:

- Risk a small, fixed fraction per trade. Many educators suggest risking no more than 1–2% of account equity on any single position. Size your

Lotsso the ATR-based stop distance stays within that limit. - Test on a demo account first. Run the EA on a demo or in the Strategy Tester across multiple market conditions before considering any live capital. This lets you observe its behavior without financial exposure.

- Understand drawdown. Every strategy endures losing streaks. Know the historical maximum drawdown you are willing to tolerate and how a run of consecutive losses would affect your account and your discipline.

- Account for costs. Spreads, commissions, and slippage all erode results, especially for an intraday system that may trade around volatile breakouts. The

MaxSpreadPointsfilter helps, but real-world execution still differs from a backtest. - Never over-leverage. Leverage magnifies both gains and losses. Keep position sizes conservative relative to your account, and never trade with money you cannot afford to lose.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: CamarillaBreakoutContinuation.ex5 (1 downloads)

- Source Code: CamarillaBreakoutContinuation.mq5 (1 downloads)

- Documentation: CamarillaBreakoutContinuation.pdf (0 downloads)