Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

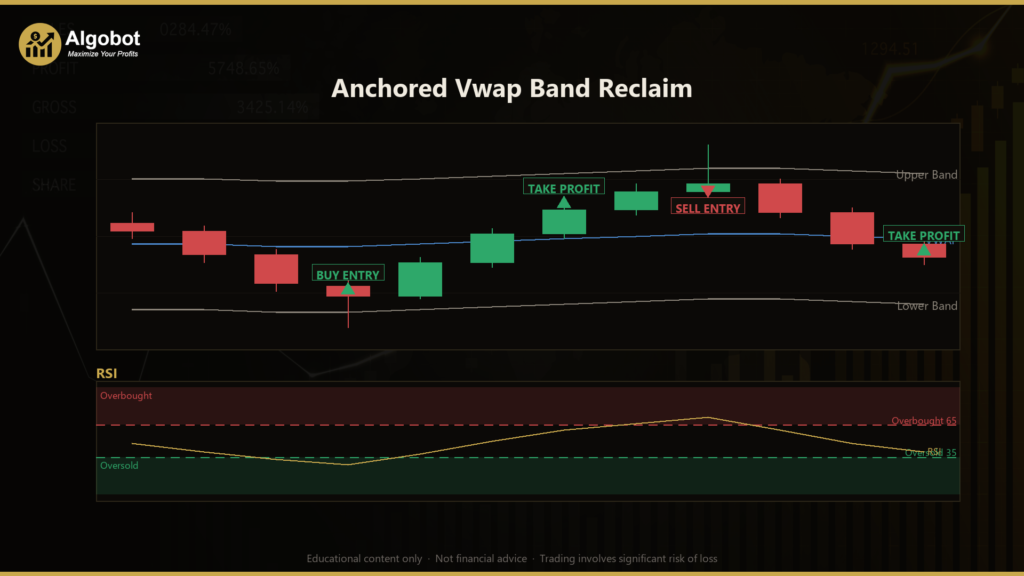

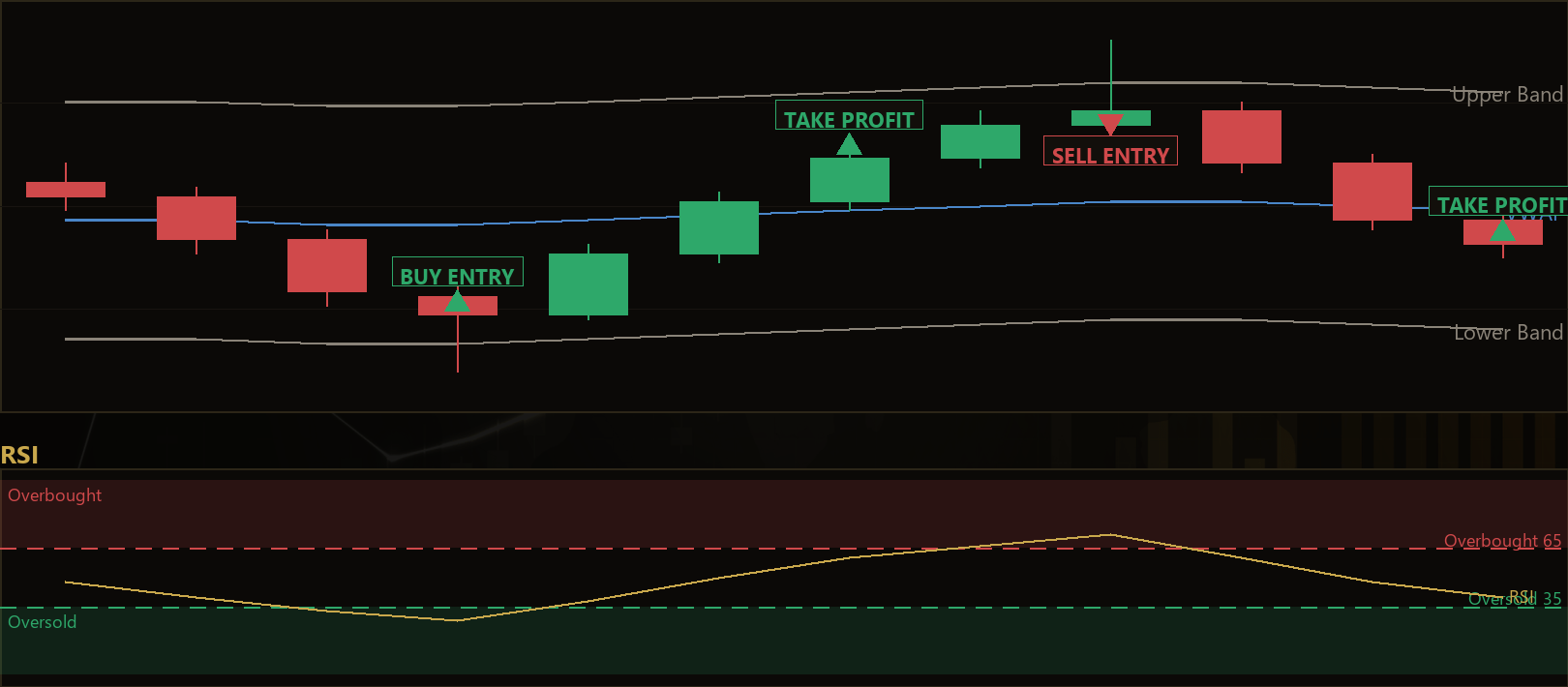

The Anchored Vwap Band Reclaim strategy is an intraday mean-reversion scalper built around the session-anchored VWAP (Volume-Weighted Average Price) — the running benchmark that institutional trading desks use to measure where the average participant has actually filled their orders during the day. Rather than chasing momentum, this strategy fades over-stretched moves, looking for moments when price has been pushed too far from its session "fair value" and then snaps back. It combines three classic building blocks: VWAP as the value anchor, the Relative Strength Index (RSI, a momentum oscillator) as a confirmation filter, and a candlestick rejection (a price-action pin-bar pattern) as the actual trigger.

The approach is designed for range-bound and balanced intraday conditions — the kind of two-sided, mean-reverting market where price oscillates around a central value rather than trending strongly in one direction. When a candle stretches beyond a statistical deviation band and then closes back inside it with a long rejection wick, the strategy interprets that as the market rejecting an extreme price. The session-anchored VWAP resets at the start of each new UTC trading day, so the value reference is rebuilt fresh every session, just as a desk would track it.

As a learning tool, the Anchored Vwap Band Reclaim is well suited to traders who want to study how volume-weighted value, momentum exhaustion, and candlestick rejection can be layered into a single, rules-based system. It is a strategy analysis exercise in confluence — no single signal acts alone; all three must align. This article explains how those pieces fit together so you can learn the mechanics, not so you can expect any particular financial outcome.

How It Works

The strategy acts once per newly-closed bar on the selected timeframe. It continuously rebuilds the session-anchored VWAP and its deviation bands, then waits for a precise rejection pattern to form. Here is how the logic flows:

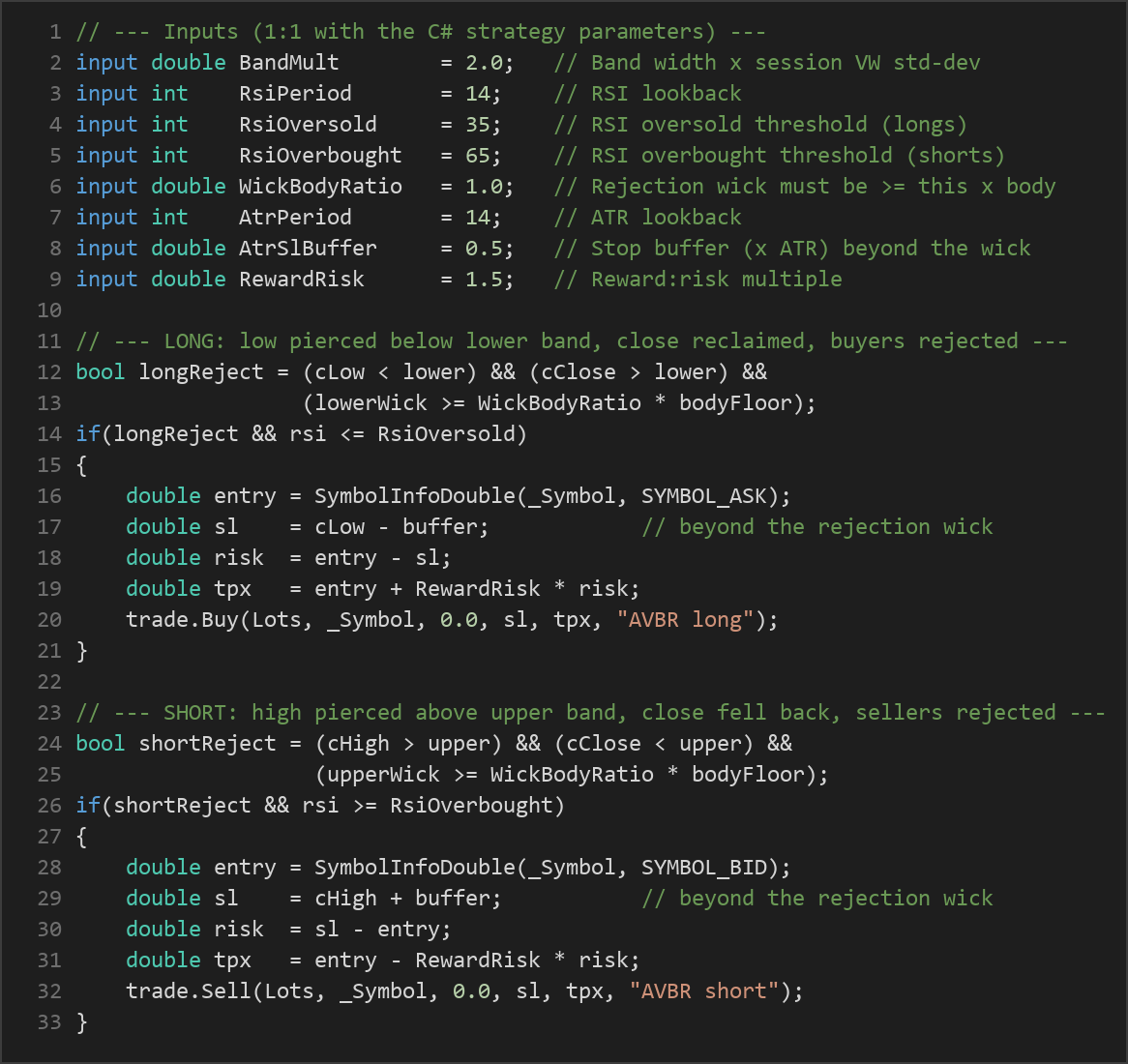

- Anchoring the VWAP: From the start of each UTC day, the strategy accumulates the typical price

(High + Low + Close) / 3weighted by each bar's tick volume. From this it derives the session VWAP and the volume-weighted standard deviation of price around it. - Building the bands: An upper and lower band are placed at

VWAP ± (BandMult × standard deviation). Because the deviation is recalculated each bar, the bands automatically widen on volatile days and narrow on quiet ones. - Warm-up filter: The strategy ignores the early session until at least

MinSessionBarsbars have accumulated, so it never trades against an unsettled, thinly-anchored VWAP. - Long rejection signal: The strategy signals a potential long when the just-closed candle's low pierces below the lower band but its close reclaims back above it, and the lower (rejection) wick is at least

WickBodyRatiotimes the candle body. This describes buyers slamming an over-stretched move back inside value. - Short rejection signal: Symmetrically, a potential short is signaled when the candle's high pierces above the upper band but the close falls back below it, with an upper rejection wick at least

WickBodyRatiotimes the body — sellers rejecting the stretch. - RSI confirmation: A rejection only counts when momentum is exhausted. For longs, RSI must be at or below

RsiOversold; for shorts, RSI must be at or aboveRsiOverbought. This filters out rejections that occur while momentum is still strong. - Spread and position filters: No new entry is taken if the current spread exceeds

MaxSpreadPoints, and only one position per magic number is held at a time so each trade is managed in isolation.

For exits, the strategy uses a fixed ATR-based reward-to-risk scalp (ATR is the Average True Range, a volatility measure):

- Stop-loss logic: The stop is placed one ATR buffer beyond the rejection wick — below the candle's low for longs, above the candle's high for shorts. The buffer size is

AtrSlBuffer × ATR. This sits at the price level where the rejection idea would be proven wrong. - Take-profit logic: The target is set at a

RewardRiskmultiple of the measured stop distance. If the stop is 10 points away andRewardRiskis 1.5, the target sits 15 points from entry. - Trade management: Once placed, the structural stop and fixed target manage the trade entirely. There is no trailing or scaling — each position runs to one outcome or the other.

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| BandMult | 2.0 | 1.0 | 4.0 | Band width as a multiple of the session volume-weighted standard deviation. Higher values demand a larger stretch before a signal. |

| RsiPeriod | 14 | 5 | 30 | Lookback length for the RSI momentum filter. |

| RsiOversold | 35 | 10 | 45 | RSI threshold a long rejection must be at or below to confirm momentum exhaustion. |

| RsiOverbought | 65 | 55 | 90 | RSI threshold a short rejection must be at or above to confirm momentum exhaustion. |

| WickBodyRatio | 1.0 | 0.3 | 3.0 | Minimum size of the rejection wick relative to the candle body (pin-bar quality filter). |

| AtrPeriod | 14 | 5 | 30 | Lookback length for the ATR used to size the stop buffer. |

| AtrSlBuffer | 0.5 | 0.0 | 2.0 | Stop buffer as a multiple of ATR, placed beyond the rejection wick. |

| RewardRisk | 1.5 | 0.5 | 4.0 | Reward-to-risk multiple that sets the take-profit distance relative to the stop. |

| MinSessionBars | 8 | 3 | 60 | Number of bars that must anchor the VWAP before any entry is allowed. |

| MaxSpreadPoints | 80 | 5 | 300 | Maximum spread (in points) allowed for a new entry; wider spreads are skipped. |

| Lots | 0.10 | 0.01 | 1.0 | Trade volume in lots. |

| Magic | 5187 | 0 | 9,999,999 | Unique identifier so the EA only manages its own positions. |

Recommended Chart Settings

The Anchored Vwap Band Reclaim was designed for liquid FX majors or indices — such as EURUSD, US500, or US100 — on lower intraday timeframes (M1 to M15), the natural home of anchored-VWAP reversion scalping. These instruments offer the tight spreads and consistent intraday volume that a VWAP-based approach depends on. The strategy uses only the primary timeframe selected at backtest time, so the timeframe you attach it to is the one it trades.

Keep in mind that VWAP behavior, volatility, and rejection frequency differ across symbols and sessions. Results will vary across different market conditions, and a setting that looks reasonable on one instrument or session may behave very differently on another. Treat these as starting points for study rather than fixed recommendations.

How to Install on MetaTrader 5

- Download the .ex5 file from the link below.

- Copy it to your MT5

MQL5\Expertsfolder. - Restart MetaTrader 5 or refresh the Navigator panel.

- Drag the EA onto a chart matching the recommended symbol and timeframe.

- Configure the input parameters and enable Algo Trading.

What to Consider Before Using This EA

Every strategy involves trade-offs, and understanding them is part of learning to evaluate a system honestly.

Strengths of this approach. The strategy is built on confluence: a price-action rejection, a statistical deviation band, and a momentum filter all have to agree before a trade is signaled, which historically reduces low-quality entries. The session-anchored VWAP gives it a meaningful, institutionally-recognized reference point rather than an arbitrary moving average. Its risk is structurally defined — the stop sits where the rejection thesis is invalidated — and the ATR-based sizing lets the stop adapt to current volatility.

Known limitations. Mean-reversion strategies are, by design, vulnerable to strong trends. When a market breaks out and runs, price can poke through a band, trigger a rejection signal, and keep going — the very scenario that produces losing trades for a fader. The RSI and band filters reduce but cannot eliminate this. The strategy also depends on tick-volume quality, which is a proxy for real volume in decentralized FX; on illiquid symbols or thin sessions this can distort the VWAP. Lower timeframes mean spread and slippage matter more, which is why the MaxSpreadPoints filter exists.

Where it may underperform. Expect the strategy to struggle during trending or news-driven expansion days, during the unsettled early minutes of a session before the VWAP anchors, and on instruments with wide or erratic spreads. It is most at home in balanced, two-sided, range-bound conditions. No parameter set makes it universally robust — this is a tool for studying mean-reversion mechanics, not a finished answer.

Risk Management Tips

Sound risk management matters far more than any single entry signal. As you study this strategy, keep these general principles in mind:

- Risk a small, fixed fraction per trade. A common educational guideline is to risk no more than 1–2% of account equity on any single position, sizing your lots so the distance to the stop equals that fraction.

- Test on a demo account first. Run the strategy in a simulated environment across many sessions and market conditions before considering any live use, so you understand its behavior without financial exposure.

- Understand drawdown. Even a well-designed mean-reversion system experiences losing streaks. Study the depth and length of historical drawdowns so you know what a normal rough patch looks like and can avoid abandoning or over-leveraging a system at the wrong time.

- Account for costs. Spread, commission, and slippage compound quickly on a low-timeframe scalper. Factor them into any evaluation rather than assuming frictionless fills.

- Never trade money you cannot afford to lose, and treat every parameter as a hypothesis to be tested, not a guarantee.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: AnchoredVwapBandReclaim.ex5 (5 downloads)

- Source Code: AnchoredVwapBandReclaim.mq5 (4 downloads)

- Documentation: AnchoredVwapBandReclaim.pdf (6 downloads)