Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

The Adaptive Transition Matrix Bias strategy is a self-learning, statistics-driven Expert Advisor (EA) built around a 3-state Markov chain — a probability model that estimates how likely the next event is, given only the current one. Rather than relying on classic indicators, chart patterns, or support-and-resistance levels, it converts each completed price bar into a single discrete symbol (UP, DOWN, or FLAT) and studies how those symbols follow one another over time. The only conventional tool it uses is the Average True Range (ATR), a volatility measure, and even that serves purely as a yardstick for "meaningful movement" — never as a buy or sell signal on its own.

The core idea is simple to state. If prices were a perfectly random walk, knowing today's bar would tell you nothing about tomorrow's. This strategy tests the opposite hypothesis: that real order flow leaves a short, shifting "memory" in the sequence of bars, so that the current bar's character carries a small, measurable bias about the next bar's likely direction. The EA continuously measures that bias and only acts when it is statistically strong enough to stand out from noise.

As a learning tool, the Adaptive Transition Matrix Bias is best suited to intermediate and advanced traders who are curious about quantitative, regime-adaptive modelling and want to study how a market can be reduced to a stream of states. It is designed for liquid markets on intraday timeframes, and it is offered here as a strategy analysis — a way to explore probability-based thinking — rather than as a shortcut to results.

How It Works

The strategy processes data once per completed bar (never mid-bar), which keeps every decision causal and free of look-ahead bias. Here is the step-by-step logic in plain English:

- Classify each bar into a state. The EA measures the bar's body (Close minus Open). It compares that body against a "dead-zone" equal to

FlatZoneAtr × ATR. If the body is larger than the dead-zone it is UP; smaller than the negative dead-zone it is DOWN; anything in between is FLAT (no meaningful effort). - Update a learning matrix. The EA keeps a 3×3 grid of recency-weighted counts recording how often each state was followed by each other state. On every new bar the whole grid is multiplied by

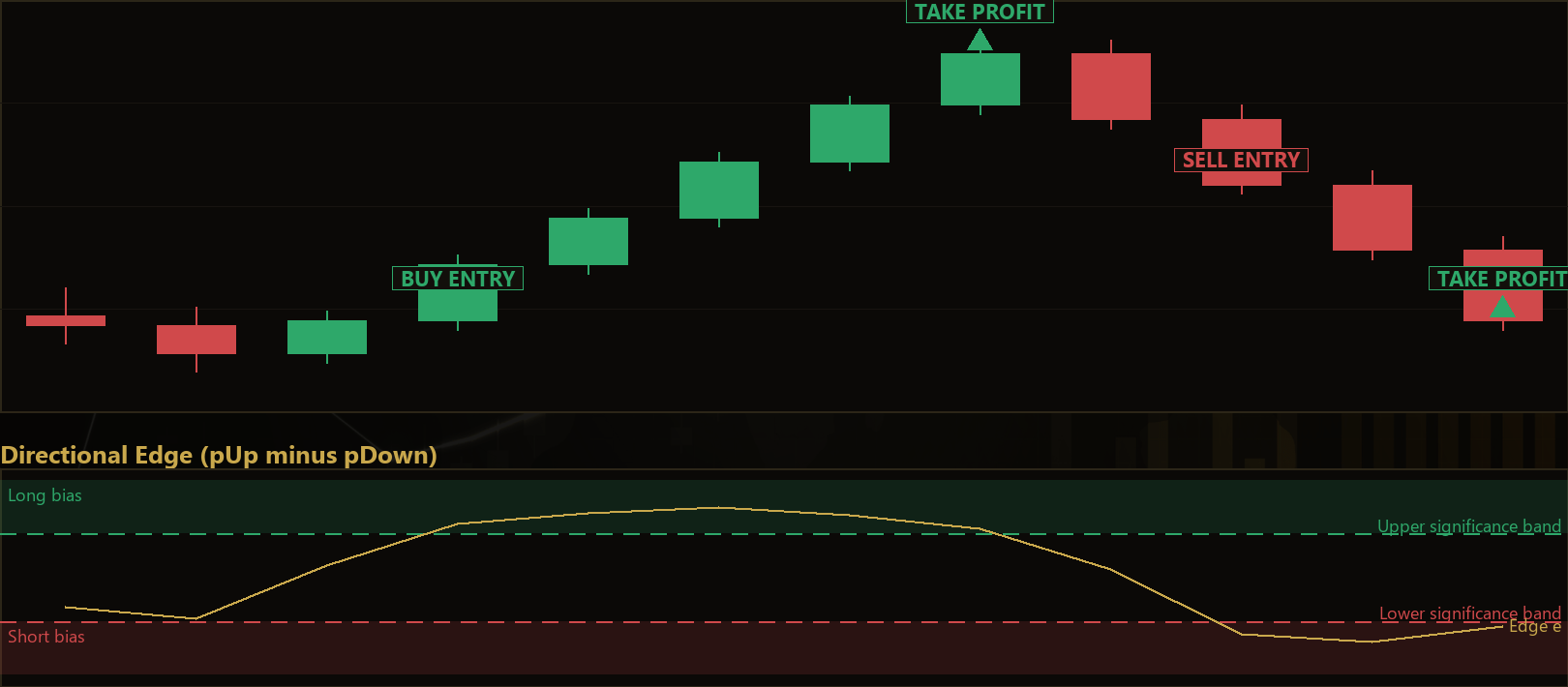

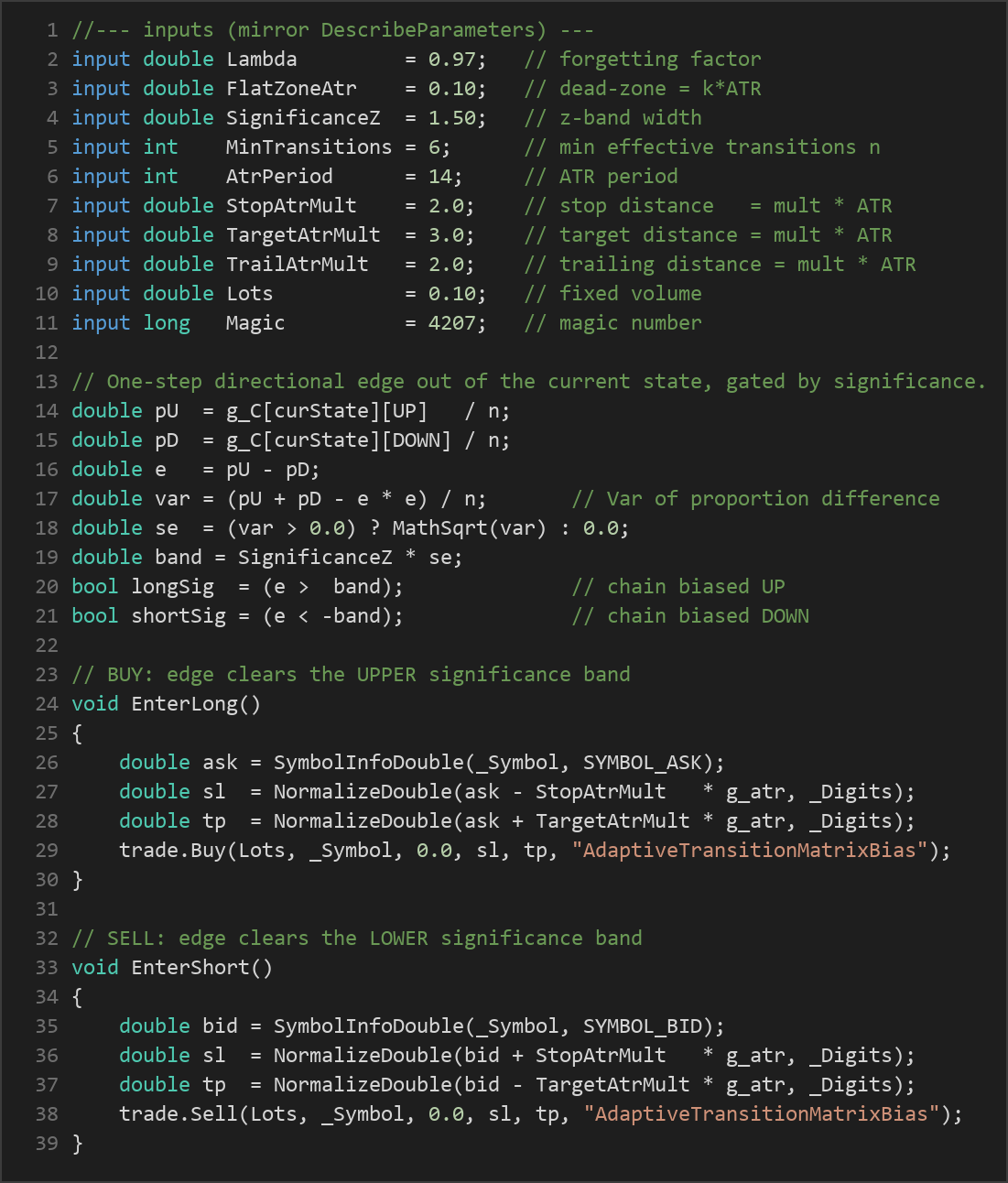

Lambda(a forgetting factor), then the newest transition is added. This "exponential forgetting" lets the model track the current regime and gradually forget stale behaviour. - Read the directional edge. From the row belonging to the current state, the EA calculates the probability of the next bar being UP (

pU) versus DOWN (pD). The difference,e = pU − pD, is the one-step directional edge — a number between −1 and +1. - Apply a self-adapting significance gate. Because

eis estimated from a limited sample, the EA computes its statistical uncertainty (a standard error) and demands that the edge clearSignificanceZstandard errors, and that at leastMinTransitionsobservations exist. When the sample is small, a large edge is required; once many consistent transitions accumulate, a smaller persistent edge is accepted. - Entry — the strategy signals a long when the edge is significantly positive (

e > z × SE), and signals a short when the edge is significantly negative (e < −z × SE). The trade enters at the open of the next bar. - Stop-loss logic. On a long, the stop is placed at

StopAtrMult × ATRbelow entry; on a short, the same distance above entry. The stop distance scales automatically with current volatility. - Take-profit logic. The target is placed at

TargetAtrMult × ATRaway from entry in the trade's favour. - Trailing stop. If

TrailAtrMultis greater than zero, an ATR-based trailing stop follows price but only ratchets in the trade's favour — it never loosens. - Adaptive flip-exit. If the learned edge reverses against an open position (a long while the chain flips down, or a short while it flips up), the EA closes the trade early. This is an adaptive exit that reacts to a detected regime change, independent of the fixed stop.

- One position per Magic number is allowed at any time, keeping exposure controlled.

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| Lambda | 0.97 | 0.90 | 0.995 | Forgetting factor. Higher values keep a longer memory (~1/(1−Lambda) bars); lower values adapt faster to new regimes. |

| FlatZoneAtr | 0.10 | 0.00 | 0.50 | Width of the volatility dead-zone as a multiple of ATR. Larger values classify more bars as FLAT. |

| SignificanceZ | 1.50 | 0.50 | 3.00 | How many standard errors the edge must clear before a trade is allowed. Higher = stricter, fewer signals. |

| MinTransitions | 6 | 3 | 20 | Minimum number of effective observations required before the model will act on a state's row. |

| AtrPeriod | 14 | 5 | 40 | Lookback length for the ATR volatility measure used in dead-zone and risk sizing. |

| StopAtrMult | 2.0 | 0.5 | 5.0 | Stop-loss distance as a multiple of ATR. |

| TargetAtrMult | 3.0 | 0.5 | 8.0 | Take-profit distance as a multiple of ATR. |

| TrailAtrMult | 2.0 | 0.0 | 6.0 | Trailing-stop distance as a multiple of ATR. Set to 0 to disable trailing. |

| Lots | 0.10 | 0.01 | 1.0 | Fixed trade volume in lots. |

Recommended Chart Settings

The Adaptive Transition Matrix Bias was designed with a liquid FX major such as EUR/USD in mind, on an intraday timeframe (M15 or H1). These conditions provide the clean, high-frequency stream of bars the Markov model needs to build reliable transition statistics. That said, the code locks to no specific timeframe — it runs on whatever chart it is attached to.

Because the model learns from recent behaviour, its output will vary considerably across different symbols, timeframes, and market conditions. Trending phases and mean-reverting phases produce very different transition matrices, so you should expect the strategy's character to change as the market changes. Always study its behaviour on a demo account across a range of conditions before drawing any conclusions.

How to Install on MetaTrader 5

- Download the .ex5 file from the link below

- Copy it to your MT5

MQL5\Expertsfolder - Restart MetaTrader 5 or refresh the Navigator panel

- Drag the EA onto a chart matching the recommended symbol and timeframe

- Configure the input parameters and enable Algo Trading

What to Consider Before Using This EA

Strengths. The most interesting quality of this approach is that it is genuinely adaptive. The forgetting factor lets the transition matrix track the current regime, and the significance gate scales its demands to the amount of evidence available. There are no fixed price thresholds anywhere — every decision rescales itself to volatility and to the statistical confidence in the sample. The flip-exit adds a second, independent way out of a trade when conditions change, which can help the strategy respond to sudden regime shifts.

Known limitations. A Markov model of this kind assumes there is a stable, exploitable short-memory structure to capture. Markets frequently behave close to random, and during those stretches the significance gate may block trades for long periods — which is by design, but can feel inactive. When a regime shifts abruptly, the forgetting factor needs time to relearn, and trades taken during that transition may underperform. The three-state simplification also discards a great deal of information (wick size, volume, gaps), so the model sees only a coarse summary of price action.

Where it may struggle. Choppy, low-volatility ranges can produce many FLAT bars and unstable estimates, while news-driven spikes can distort the ATR and the transition counts at the same time. Very wide spreads or illiquid symbols will erode the ATR-scaled edges the model relies on. Treat this EA as a framework for studying regime-adaptive probability, not as a finished, plug-and-play system.

Risk Management Tips

Sound risk management matters far more than any single strategy. Consider these general principles as you study this EA:

- Position sizing: Keep trade size proportionate to your account. Many educators suggest risking no more than 1–2% of account equity per trade so that a losing streak does not cause severe damage.

- Use a demo account first: Test the strategy on a demo or simulated account until you understand its behaviour across trending and ranging conditions.

- Understand drawdown: Every strategy experiences losing periods. Study the depth and duration of drawdowns so your expectations are realistic before risking real capital.

- Respect the stop-loss: The ATR-based stop is central to this design. Disabling or widening it removes the protection it was built to provide.

- Diversify and stay informed: Avoid concentrating all risk in a single instrument or a single automated system, and keep an eye on major economic events that can disrupt any model.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: AdaptiveTransitionMatrixBias.ex5 (0 downloads)

- Source Code: AdaptiveTransitionMatrixBias.mq5 (0 downloads)

- Documentation: AdaptiveTransitionMatrixBias.pdf (0 downloads)