Disclaimer: This article is for educational and informational purposes only. It does not constitute financial or investment advice. Trading forex and CFDs carries significant risk of loss. Past performance of any strategy — including backtests — does not guarantee future results. Never trade with money you cannot afford to lose.

What Is This Strategy?

The Adaptive Efficiency Trend Rider is a trend-following pullback strategy built around Kaufman's Adaptive Moving Average (KAMA) — a moving average that automatically changes how quickly it reacts to price based on how efficiently the market is moving. Unlike a plain simple or exponential moving average, which uses one fixed speed regardless of conditions, KAMA speeds up when price travels in a clean, one-directional trend and slows down when price chops sideways. This single adaptive characteristic is what the whole strategy is designed around.

The core idea comes from the efficiency ratio (ER), a number between 0 and 1 that measures how much net directional progress price has made compared to the total distance it actually travelled. An ER near 1 means the market covered ground in a straight, efficient line (a strong trend). An ER near 0 means price wandered back and forth without going anywhere (noise). KAMA uses the ER to decide its own smoothing speed, so the strategy naturally becomes more responsive in trends and more sluggish — and therefore quieter — in ranges.

As a learning tool, the Adaptive Efficiency Trend Rider is well suited to traders who want to understand adaptive indicators, pullback entries, and multi-condition confirmation. It is conceived for trending forex, index, and metal charts on intermediate timeframes such as M15 to H4. This is a strategy analysis intended to help you study how adaptive filtering, momentum confirmation, and volatility-based risk sizing fit together — not a shortcut to any particular outcome.

How It Works

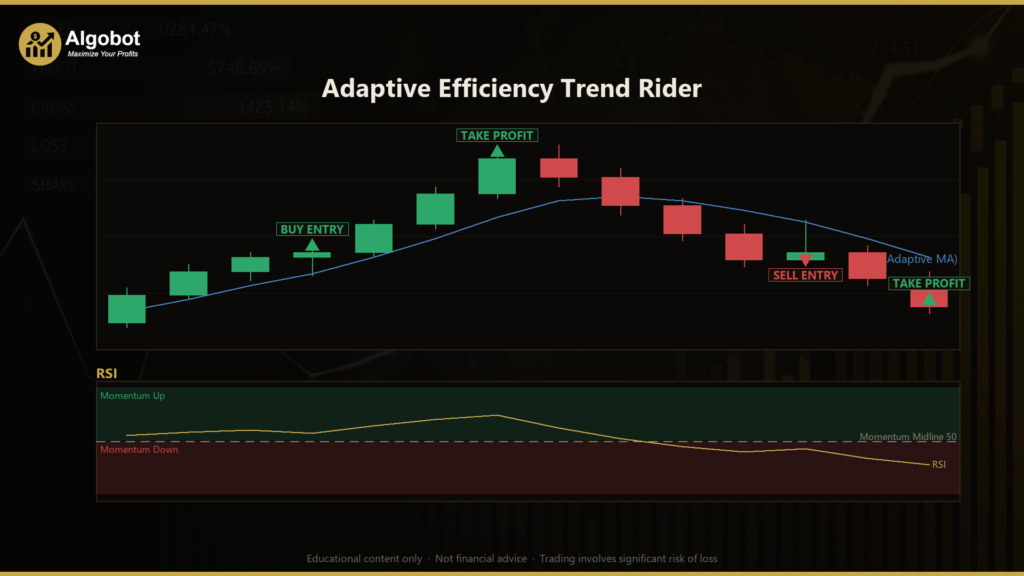

The strategy evaluates its rules only on the just-closed bar, so signals are confirmed rather than based on a still-forming candle. The adaptive KAMA line does double duty: its slope acts as the trend filter, and the line's price level acts as the dynamic pullback zone the strategy wants price to reclaim.

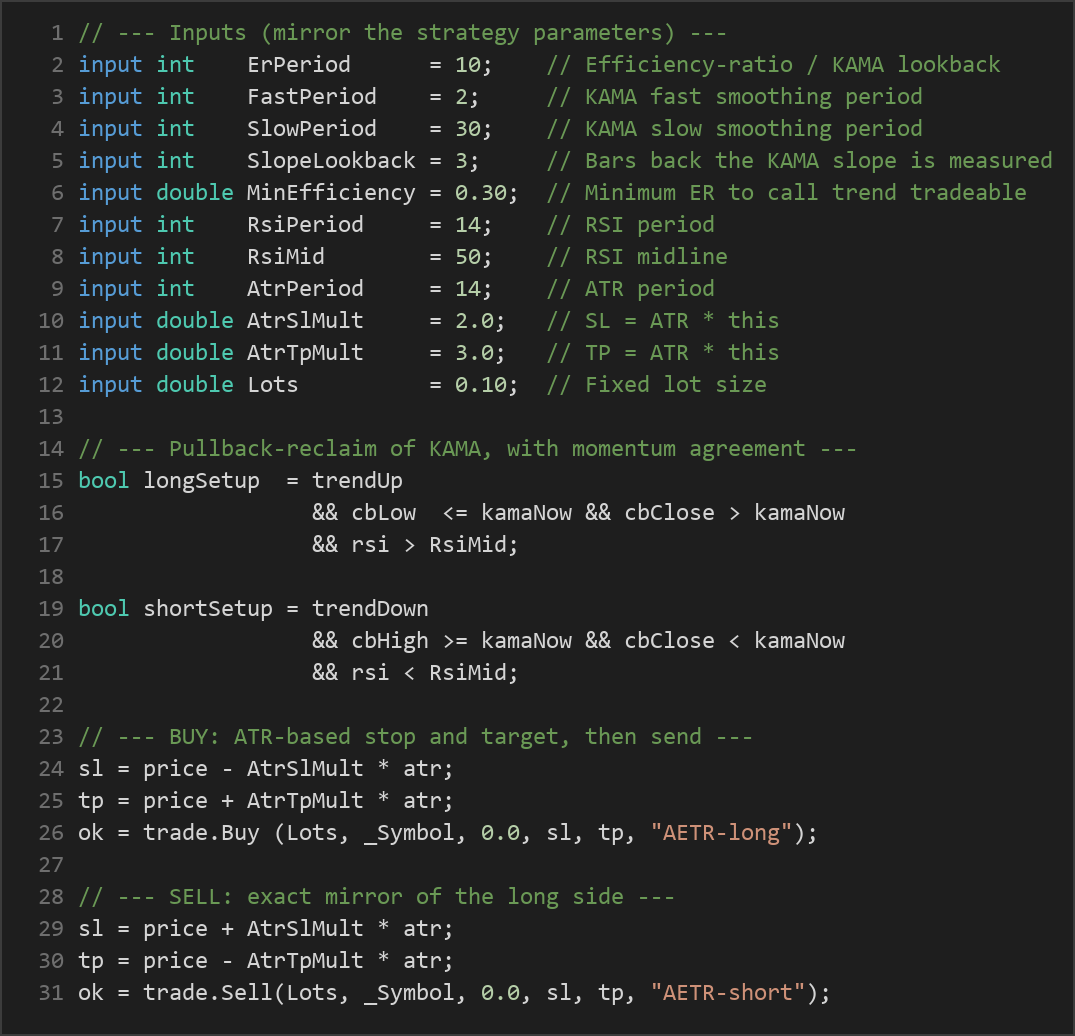

The strategy signals a long entry when all of these conditions hold on the closed bar:

- Adaptive uptrend: KAMA is higher now than it was

SlopeLookbackbars ago (the adaptive line is rising). - Efficient trend: the efficiency ratio is at or above

MinEfficiency, meaning the trend is moving with genuine directional conviction rather than merely drifting. - Pullback and reclaim: the bar's low dipped to or through the KAMA line (

Low <= KAMA), yet the bar closed back above it (Close > KAMA). This captures a shallow dip that was bought back before the close. - Momentum agreement: the Relative Strength Index (RSI) — a 0-to-100 momentum oscillator — is above the

RsiMidmidline, confirming momentum still leans upward.

A short entry is the exact mirror image: KAMA falling over the lookback, ER at or above the minimum, the bar's high poking above KAMA while the close finishes below it, and RSI below the midline.

Exit, stop-loss, and take-profit logic:

- Risk is defined using the Average True Range (ATR), an indicator that measures recent volatility, so stops and targets adapt to how active the market currently is.

- The stop-loss is placed

AtrSlMult× ATR away from entry (below entry for longs, above for shorts). - The take-profit is placed

AtrTpMult× ATR away from entry (above for longs, below for shorts). - With the default multipliers (stop at 2× ATR, target at 3× ATR), the target sits at a 1.5:1 reward-to-risk ratio.

- Only one position per magic number is allowed open at a time, so the strategy does not stack multiple trades on the same signal.

- A trade is skipped if the calculated stop distance is degenerate (zero or negative) or if ATR is not positive, avoiding malformed orders.

Because KAMA flattens automatically when the market turns noisy, the rising/falling slope filter goes quiet in ranges — which is exactly where simple moving-average pullback systems tend to generate their weakest signals. The efficiency and reclaim filters are layered on top to further screen out low-quality setups.

Strategy Parameters

| Parameter | Default | Min | Max | Description |

|---|---|---|---|---|

| ErPeriod | 10 | 5 | 20 | Lookback window (in bars) for the efficiency ratio and KAMA calculation. |

| FastPeriod | 2 | 2 | 6 | KAMA's fastest smoothing period, used when the market is highly efficient. |

| SlowPeriod | 30 | 15 | 50 | KAMA's slowest smoothing period, used when the market is noisy. |

| SlopeLookback | 3 | 1 | 8 | How many bars back the KAMA slope (trend direction) is measured over. |

| MinEfficiency | 0.30 | 0.10 | 0.70 | Minimum efficiency ratio (0–1) required to consider the trend tradeable. |

| RsiPeriod | 14 | 7 | 21 | Number of bars used to calculate the RSI momentum oscillator. |

| RsiMid | 50 | 40 | 60 | RSI midline; longs require RSI above it, shorts require RSI below it. |

| AtrPeriod | 14 | 7 | 28 | Number of bars used to calculate ATR for stop and target sizing. |

| AtrSlMult | 2.0 | 1.0 | 4.0 | Stop-loss distance as a multiple of ATR. |

| AtrTpMult | 3.0 | 1.0 | 6.0 | Take-profit distance as a multiple of ATR. |

| Lots | 0.10 | 0.01 | 1.0 | Fixed trade size in lots. |

Recommended Chart Settings

The Adaptive Efficiency Trend Rider was conceived for trending instruments — major forex pairs, stock indices, and metals such as gold — on intermediate timeframes from M15 to H4. These timeframes tend to produce the kind of sustained, efficient moves the KAMA slope and efficiency filters are designed to detect, while filtering out much of the intrabar noise found on very short charts.

The strategy reads its timeframe from whatever chart it is attached to, so it is not hardcoded to a single period; you choose the timeframe at test time. Keep in mind that results will vary significantly across different symbols, timeframes, and market conditions. An instrument that trends cleanly in one period may spend the next in a choppy range where the efficiency filter correctly keeps the strategy on the sidelines. Always study behaviour across a range of conditions before drawing conclusions.

How to Install on MetaTrader 5

- Download the .ex5 file from the link below

- Copy it to your MT5

MQL5\Expertsfolder - Restart MetaTrader 5 or refresh the Navigator panel

- Drag the EA onto a chart matching the recommended symbol and timeframe

- Configure the input parameters and enable Algo Trading

What to Consider Before Using This EA

Strengths of the approach. The biggest conceptual advantage is that KAMA adapts on its own. In efficient trends it reacts quickly and rides the move; in noise it flattens and the slope filter naturally stands aside. Layering the explicit efficiency-ratio threshold, the pullback-and-reclaim requirement, and RSI momentum confirmation on top means several independent conditions must agree before a trade is taken, which is designed to cut the low-quality entries that plain moving-average crossover systems often take. The ATR-based stops and targets also let risk scale with volatility rather than using fixed distances.

Known limitations. Every trend-following method — adaptive or not — struggles in prolonged sideways markets. Although the efficiency filter reduces range-bound trading, no filter is perfect, and false pullback signals can still occur near the edges of a range. Adaptive indicators can also lag at sharp reversals: KAMA needs a few bars of clean movement before its slope confirms a new direction, so the earliest part of a fresh trend may be missed. Because the strategy requires multiple simultaneous conditions, it may also produce relatively few signals, which some traders find requires patience.

Where it may underperform. Consider low-volatility, choppy conditions, news-driven whipsaws, and instruments that mean-revert rather than trend. The fixed 1.5:1 reward-to-risk profile means the historical win rate needs to stay high enough to offset losing trades; if market character shifts, that balance can erode. Parameter choices such as MinEfficiency, SlopeLookback, and the ATR multipliers materially change behaviour, so treat the defaults as a starting point for study, not a finished configuration.

Risk Management Tips

Sound risk management matters more than any single indicator setting. Consider these general principles as part of your education:

- Position sizing: size trades so that a full stop-loss represents only a small, pre-decided fraction of your account. A common guideline among educators is to risk no more than 1–2% of account equity per trade.

- Respect the stop: the ATR-based stop exists to define your risk before you enter. Avoid widening or removing it once a trade is live.

- Test on a demo account first: run the strategy on a demo or in the Strategy Tester across varied market conditions before ever considering real capital.

- Understand drawdown: every strategy experiences losing streaks. Know the historical drawdown you might face and ask honestly whether you could tolerate it emotionally and financially.

- Diversify and stay realistic: avoid concentrating risk in a single instrument or a single strategy, and keep expectations grounded — no configuration removes the possibility of loss.

Risk Warning

Trading foreign exchange, CFDs, and other leveraged financial instruments involves substantial risk of loss and is not suitable for all investors. The strategies and tools discussed on this page are provided for educational purposes only and do not constitute financial advice, investment recommendations, or solicitation to trade. Always consult a qualified financial adviser before making trading decisions. Past backtest performance is not indicative of future results.

Downloads

- Expert Advisor: AdaptiveEfficiencyTrendRider.ex5 (2 downloads)

- Source Code: AdaptiveEfficiencyTrendRider.mq5 (3 downloads)

- Documentation: AdaptiveEfficiencyTrendRider.pdf (3 downloads)